Mastering the 2026 PSLF Program: Your 10-Year Eligibility Guide

Student loan debt can feel like a heavy burden, but for those dedicated to public service, the Public Service Loan Forgiveness (PSLF) program offers a beacon of hope. Established in 2007, PSLF promises to forgive the remaining balance on federal direct loans after 120 qualifying monthly payments while working full-time for a qualifying employer. As we approach 2026, many early participants in the program will be reaching their 10-year eligibility mark, making now a crucial time to understand the nuances of this life-changing opportunity. This comprehensive guide will walk you through everything you need to know about 2026 PSLF Eligibility, ensuring you are well-prepared to claim the forgiveness you’ve earned.

Understanding the Core of PSLF: What is it, and Who is it For?

The Public Service Loan Forgiveness (PSLF) program was created to encourage individuals to enter and remain in public service jobs. It provides a pathway to debt relief for those who commit a decade of their careers to serve their communities. Essentially, if you work full-time for a qualifying employer and make 120 qualifying monthly payments under an income-driven repayment (IDR) plan, your remaining federal direct loan balance can be forgiven, tax-free.

Who Qualifies for PSLF?

PSLF is specifically designed for individuals working in public service. This broadly includes:

- Government Organizations: Federal, state, local, or tribal government organizations, including the military.

- 501(c)(3) Non-Profit Organizations: Tax-exempt non-profit organizations.

- Other Non-Profit Organizations: Certain other non-profit organizations that provide specific public services, such as public health, public safety, or education.

It’s important to note that the type of job you do for these organizations generally doesn’t matter, as long as it’s full-time. What matters is who your employer is. For-profit organizations, labor unions, and partisan political organizations do not qualify.

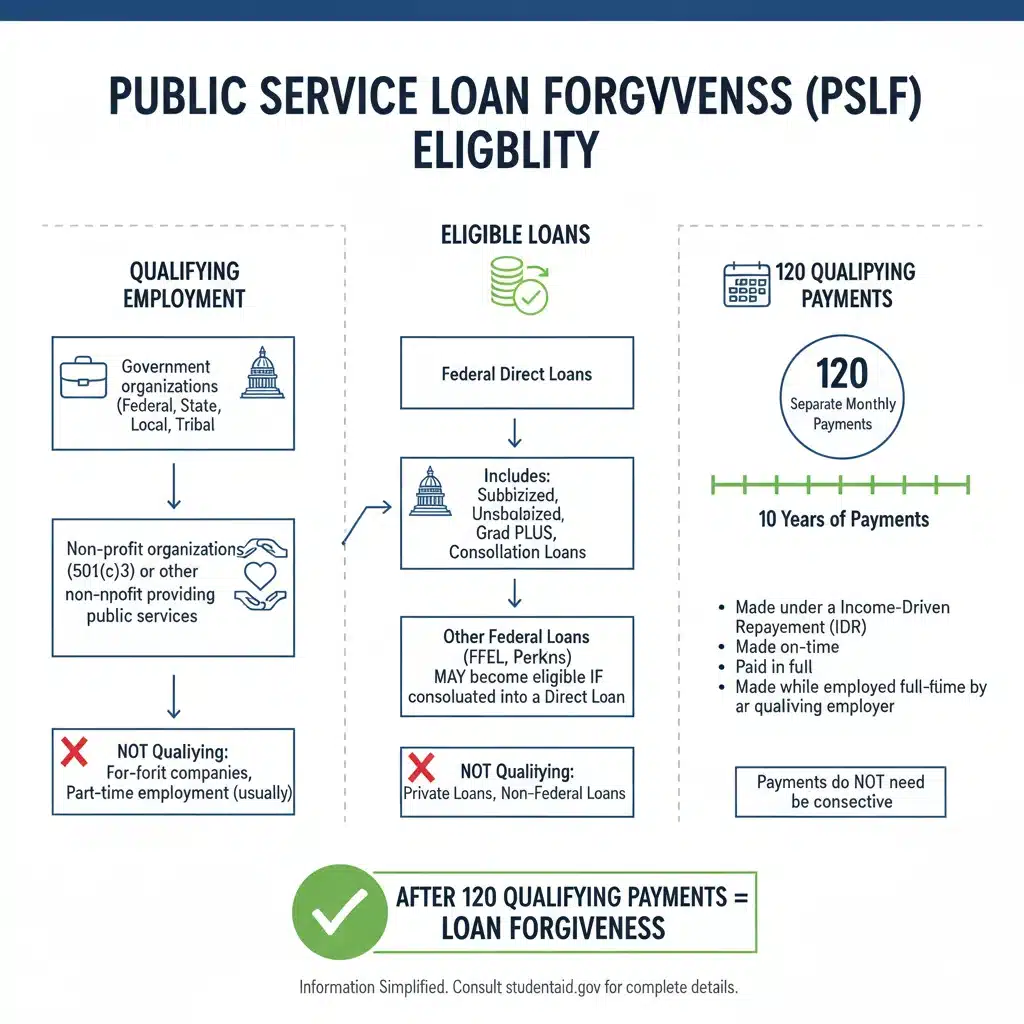

The Three Pillars of 2026 PSLF Eligibility: A Deep Dive

To successfully achieve loan forgiveness through PSLF, you must meet three fundamental requirements simultaneously for 10 years (120 qualifying payments). These are: qualifying loans, qualifying employment, and qualifying payments under an eligible repayment plan.

Pillar 1: Qualifying Loans

Only certain types of federal student loans are eligible for PSLF. Specifically, these are:

- William D. Ford Federal Direct Loan (Direct Loan) Program loans: This includes Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Direct Consolidation Loans.

What if you have other federal loans, like Federal Family Education Loan (FFEL) Program loans or Federal Perkins Loans? These are not directly eligible. However, you can make them eligible by consolidating them into a Direct Consolidation Loan. It’s crucial to do this early in your repayment journey, as only payments made on the Direct Consolidation Loan after consolidation will count towards PSLF.

Pillar 2: Qualifying Employment

As mentioned, your employer must be a qualifying organization. Here’s a more detailed look:

- Full-time Employment: You must be employed full-time, which typically means working at least 30 hours per week. If you work multiple part-time jobs, each with qualifying employers, you can combine them to meet the 30-hour requirement, but each employer must be a qualifying one.

- Employer Verification: The Department of Education uses an Employer Certification Form (ECF) to verify your employment. This form should be submitted annually, or whenever you change employers, to ensure your payments are being tracked correctly. This proactive approach is vital for 2026 PSLF Eligibility.

Pillar 3: Qualifying Payments and Repayment Plans

This is often the most complex aspect of PSLF. You need to make 120 qualifying monthly payments under an eligible repayment plan. Let’s break this down:

- 120 Payments: These payments do not have to be consecutive. If you take a break from public service or your payments, you can pick up where you left off.

- Eligible Repayment Plans: You must be enrolled in an income-driven repayment (IDR) plan. These plans calculate your monthly payment based on your income and family size. The most common IDR plans include:

- Revised Pay As You Earn (REPAYE)

- Pay As You Earn (PAYE)

- Income-Based Repayment (IBR)

- Income-Contingent Repayment (ICR)

The Standard Repayment Plan is also a qualifying plan, but because it repays your loan in 10 years, there would be no remaining balance to forgive by the time you made 120 payments. Therefore, IDR plans are almost always the best choice for PSLF.

- On-Time Payments: Payments must be made on time (within 15 days of the due date).

- Full Payment Amount: Payments must be for the full amount due as shown on your bill.

- After October 1, 2007: Only payments made after October 1, 2007, count towards PSLF.

Understanding and adhering to these three pillars is paramount for anyone aiming for 2026 PSLF Eligibility.

The Importance of the PSLF Employer Certification Form (ECF)

The ECF is your most important tool for tracking your progress towards PSLF. It’s not just a recommendation; it’s a critical component of the process. By submitting this form:

- You verify your qualifying employment: The Department of Education confirms that your employer meets the PSLF criteria.

- Your qualifying payments are counted: The loan servicer reviews your payment history for the certified period and updates your qualifying payment count.

- You receive feedback: If there are any issues with your employment or payments, you’ll be notified, giving you time to correct them.

It is strongly recommended to submit an ECF annually, or whenever you change jobs. Waiting until you believe you’ve made 120 payments can lead to significant delays and potential heartbreak if there are unaddressed issues with your employment or payment history. Don’t underestimate the power of regular ECF submissions for your 2026 PSLF Eligibility journey.

Temporary Waivers and Program Changes: The Limited PSLF Waiver and IDR Adjustment

The PSLF program has undergone significant changes in recent years, largely to address historical issues with its implementation and to simplify the path to forgiveness for many borrowers. Two key initiatives worth understanding are the Limited PSLF Waiver and the Income-Driven Repayment (IDR) Adjustment.

The Limited PSLF Waiver (Expired October 31, 2022)

The Limited PSLF Waiver was a game-changer for many borrowers. It temporarily allowed past payments to count toward PSLF that would not have counted otherwise. This included:

- Payments made on FFEL and Perkins loans (after consolidation into a Direct Loan).

- Payments made under non-qualifying repayment plans.

- Payments that were late or for less than the full amount.

While the waiver officially ended on October 31, 2022, borrowers who consolidated their FFEL or Perkins loans into Direct Loans and submitted a PSLF form by that deadline are still having their accounts reviewed. If you took advantage of this waiver, ensure you keep an eye on your payment count updates, as these adjustments can take time. Even if you missed the waiver, understanding its impact helps contextualize the program’s evolution.

The IDR Adjustment (One-Time Account Adjustment)

The IDR Adjustment is another significant initiative by the Department of Education designed to correct past administrative errors and ensure borrowers receive credit for all qualifying payments. This adjustment is ongoing and will automatically provide credit for:

- Months in repayment, even if payments were not made under an IDR plan.

- Certain periods of deferment and forbearance that previously did not count.

- Payments on FFEL, Perkins, and HEAL loans after consolidation into a Direct Loan.

A key aspect of the IDR Adjustment is that it will also count payments towards PSLF for eligible borrowers. If you have older loans or periods of repayment that you believe should count, but didn’t under previous rules, this adjustment could significantly boost your payment count towards your 2026 PSLF Eligibility. The Department of Education expects to complete these adjustments for most borrowers by July 1, 2024, but complex cases may take longer. Monitoring your Federal Student Aid (FSA) account and contacting your servicer if you have questions is advisable.

Step-by-Step Guide to Maximizing Your 2026 PSLF Eligibility

Navigating PSLF can seem daunting, but by following a structured approach, you can significantly increase your chances of success. Here’s a step-by-step guide:

Step 1: Confirm Your Loans are Eligible

- Check Your Loan Type: Log in to your Federal Student Aid (FSA) account at studentaid.gov. Under ‘My Aid,’ you can see a list of all your federal student loans. Look for Direct Loans.

- Consolidate if Necessary: If you have FFEL or Perkins loans, consider consolidating them into a Direct Consolidation Loan. Remember, only payments made AFTER consolidation will count for PSLF. Do this as early as possible.

Step 2: Ensure Your Employment Qualifies

- Verify Your Employer: Use the PSLF Help Tool on studentaid.gov to check if your employer is a qualifying organization. This tool can also generate the ECF for you.

- Maintain Full-Time Status: Confirm you meet the full-time employment requirement (typically 30 hours per week).

- Submit ECF Regularly: Submit the PSLF Employer Certification Form (ECF) annually or whenever you change employers. This is the single most important proactive step you can take.

Step 3: Enroll in an Income-Driven Repayment (IDR) Plan

- Choose the Right Plan: Apply for an IDR plan (REPAYE, PAYE, IBR, or ICR) through your loan servicer or directly on studentaid.gov. The best plan for you depends on your income, family size, and loan types.

- Recertify Annually: Your IDR plan requires annual recertification of your income and family size. Missing this can lead to higher payments or temporary disqualification of payments. Set reminders!

Step 4: Make 120 Qualifying Payments

- On-Time and In Full: Ensure every payment is made on time and for the full amount due under your IDR plan.

- Track Your Progress: Review your loan servicer’s online portal for your PSLF payment tracker. If you submit ECFs regularly, this count should be updated.

Step 5: Apply for Forgiveness

- The Final Step: Once you believe you have made 120 qualifying payments, you will submit the PSLF Application for Forgiveness. This form confirms your final period of employment and requests the discharge of your remaining loan balance.

- Be Patient: The processing of forgiveness applications can take several months. Continue making payments until you receive confirmation of forgiveness.

- Student Loans: For more information on managing your student loans, explore our comprehensive guides.

Common Pitfalls to Avoid on Your PSLF Journey

While the PSLF program offers incredible benefits, it’s notorious for its complexities. Being aware of common mistakes can help you steer clear of them:

- Not Consolidating FFEL/Perkins Loans: Many borrowers mistakenly think their FFEL or Perkins loans will automatically qualify. Without consolidation into a Direct Loan, they won’t.

- Not Submitting ECFs Regularly: This is perhaps the biggest reason for PSLF denials. Waiting until the end makes it harder to correct past errors or track down old employers.

- Being in the Wrong Repayment Plan: Making payments under a non-IDR plan (other than Standard) will not count.

- Missing IDR Recertification: Failing to recertify your income annually can lead to your payments being re-calculated to a higher amount (Standard Repayment amount), and those months might not count for PSLF.

- Working for a Non-Qualifying Employer: Always double-check your employer’s eligibility. Many non-profits do not have 501(c)(3) status and therefore do not qualify.

- Voluntary Forbearance/Deferment: While some specific deferment/forbearance periods may count under the IDR Adjustment, generally, voluntary periods of non-payment do not count towards your 120 payments.

- Switching Loan Servicers: If your loan servicer changes, ensure all your PSLF documentation and payment counts transfer correctly. Keep your own records.

By actively avoiding these pitfalls, you significantly strengthen your path to 2026 PSLF Eligibility.

What to Expect as You Near 2026: The Home Stretch

For those who started their PSLF journey around 2016, 2026 marks the decade milestone. As you approach this critical point, here’s what to keep in mind:

- Final ECF Submission: Ensure your final Employer Certification Form covers your most recent employment period, right up to when you submit your forgiveness application.

- Review Your Payment Count: Thoroughly review your official PSLF payment count provided by your servicer. Compare it against your own records. If there are discrepancies, gather evidence (pay stubs, W-2s, payment confirmations) and dispute them with your servicer.

- Prepare for the Application: Familiarize yourself with the PSLF Application for Forgiveness. While similar to the ECF, it’s the final form you’ll need.

- Continue Payments Until Forgiven: Do not stop making payments once you apply for forgiveness. Continue until you receive official confirmation that your loans have been discharged. Any payments made over the 120 required will be refunded.

- Tax Implications: A significant benefit of PSLF is that the forgiven amount is NOT considered taxable income by the IRS. This is a crucial advantage compared to other forgiveness programs.

![]()

Resources and Tools for PSLF Success

The Department of Education provides several valuable resources to help you manage your PSLF journey:

- Federal Student Aid (FSA) Website (studentaid.gov): This is your primary resource. Here you can find information on your loans, use the PSLF Help Tool, apply for IDR plans, and submit ECFs.

- PSLF Help Tool: This interactive tool guides you through the process of determining employer eligibility, generating ECFs, and tracking your progress.

- Your Loan Servicer: Your servicer (currently MOHELA for most PSLF borrowers) is your direct point of contact for questions about your payments, IDR plans, and PSLF status.

- Student Loan Ombudsman: If you have disputes with your servicer that you cannot resolve, the FSA Ombudsman Group can provide assistance.

- Non-Profit Organizations: Many non-profit organizations specialize in student loan counseling and can offer personalized advice.

The Future of PSLF: What’s Next?

While the core structure of PSLF is expected to remain consistent, student loan policies are subject to change. It’s always wise to stay informed:

- SAVE Plan (ใหม่): The new Saving on a Valuable Education (SAVE) Plan is an improved IDR plan that offers lower monthly payments for many borrowers and prevents interest capitalization as long as you make your reduced payments. For many, this will be the most beneficial IDR plan for PSLF. If you’re not on SAVE, investigate if it’s right for you.

- Legislative Changes: Keep an eye on legislative developments that could impact federal student aid programs. While significant changes to existing forgiveness programs are less common, understanding the political landscape can be beneficial.

For those working towards 2026 PSLF Eligibility, continuous engagement with official resources and proactive management of your loan accounts will be key.

Conclusion: Your Path to 2026 PSLF Forgiveness

The Public Service Loan Forgiveness program represents a monumental opportunity for public servants to achieve financial freedom from student loan debt. As 2026 approaches, the focus on 2026 PSLF Eligibility becomes sharper for tens of thousands of dedicated individuals. By understanding the qualifying criteria for loans, employment, and payments, diligently submitting your Employer Certification Forms, and staying informed about program updates like the IDR Adjustment, you can confidently navigate the path to forgiveness.

Don’t leave your loan forgiveness to chance. Be proactive, keep meticulous records, and leverage the available resources. Your decade of service is a significant contribution, and PSLF is designed to honor that commitment. With careful planning and persistent effort, you can look forward to the profound relief of having your student loans forgiven, allowing you to continue your vital work in public service with one less burden.