The landscape of student loan debt in the United States is constantly evolving, bringing both challenges and opportunities for millions of borrowers. As we look towards 2026, significant updates to student loan forgiveness programs are poised to offer substantial relief to an estimated 1.5 million individuals. Understanding these changes is not just beneficial; it’s crucial for those seeking to alleviate the burden of educational debt. This comprehensive guide will delve into the latest developments, eligibility criteria, application processes, and what student loan forgiveness 2026 means for you.

For years, student loan debt has been a pressing issue, impacting economic mobility, housing decisions, and overall financial well-being. The sheer volume of outstanding student loans has prompted various administrations to explore and implement solutions aimed at providing a pathway to financial freedom for borrowers. The announcements pertaining to FSA 2026 are a testament to ongoing efforts to reform the student loan system and address the needs of those struggling with repayment.

This article aims to be your definitive resource, offering clear, actionable information on how these new programs and expanded eligibility can benefit you. Whether you’ve been diligently paying off your loans for decades, are a recent graduate, or are simply trying to navigate the complexities of federal student aid, the information presented here will be invaluable. We will break down the specifics, demystify the jargon, and empower you with the knowledge to pursue the relief you deserve. Let’s explore what student loan forgiveness 2026 has in store.

The Evolution of Student Loan Forgiveness Programs

Student loan forgiveness is not a new concept, but its scope and accessibility have undergone significant transformations. Historically, forgiveness programs were often limited to specific professions, such as public service, or confined to extreme circumstances like permanent disability. However, recent years have seen a broader approach, recognizing the widespread impact of student debt on the economy and individual lives. The initiatives leading up to student loan forgiveness 2026 reflect an ongoing commitment to refining these programs to be more inclusive and effective.

A Brief Look Back: Key Milestones

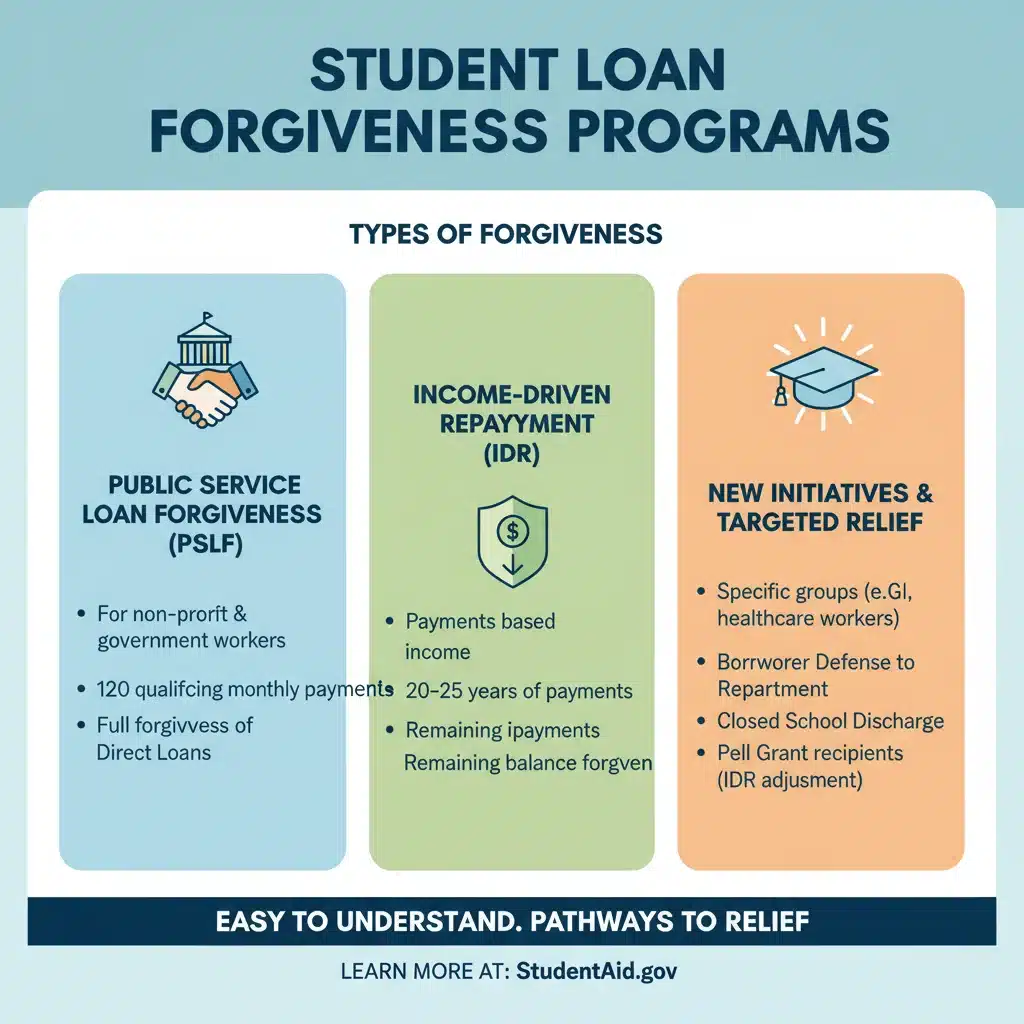

- Public Service Loan Forgiveness (PSLF): Introduced in 2007, PSLF offers forgiveness for federal direct loans after 120 qualifying monthly payments while working full-time for a qualifying employer. While impactful, it has historically faced criticism for its complex rules and low approval rates.

- Income-Driven Repayment (IDR) Plans: These plans adjust monthly payments based on a borrower’s income and family size, with any remaining balance forgiven after 20 or 25 years of payments. Recent administrative actions have focused on correcting historical miscalculations and providing retroactive relief for borrowers on these plans.

- Targeted Forgiveness Initiatives: Over the past few years, specific groups of borrowers, such as those defrauded by predatory institutions or those with total and permanent disabilities, have received targeted forgiveness.

The journey to student loan forgiveness 2026 has been marked by continuous efforts to streamline processes, expand eligibility, and address systemic issues within the federal student loan system. These ongoing reforms are culminating in the programs and relief measures that will become more prominent in the coming years, directly impacting the 1.5 million borrowers targeted for assistance.

Understanding the New Programs and Expanded Eligibility for 2026

The core of the excitement surrounding student loan forgiveness 2026 lies in the introduction of new programs and the significant expansion of eligibility for existing ones. These changes are designed to cast a wider net, ensuring that more borrowers who genuinely need assistance can access it. It’s important to differentiate between new, standalone programs and enhancements to existing frameworks, as both play a crucial role in the upcoming relief efforts.

Key Areas of Expansion and New Initiatives

- IDR Account Adjustment: A major focus leading into 2026 is the ongoing IDR account adjustment. This initiative aims to correct past administrative forbearance and deferment issues that prematurely prevented borrowers from reaching their forgiveness thresholds. Many borrowers will receive credit for periods that previously didn’t count towards forgiveness, pushing them closer, or even over, the finish line for IDR forgiveness. This adjustment is expected to be a primary driver of the 1.5 million borrowers receiving forgiveness.

- Streamlined PSLF Processes: While PSLF has been around, efforts are continually being made to simplify its application and qualification criteria. Future updates for 2026 may include more automated tracking of eligible payments and employers, reducing the administrative burden on borrowers and improving approval rates.

- Targeted Relief for Specific Groups: Beyond broad-based programs, there will likely be continued emphasis on providing relief for specific vulnerable populations. This could include further actions for borrowers with disabilities, those who attended schools that closed abruptly, or individuals facing severe financial hardship.

- Potential for New, Broader Forgiveness Frameworks: Although less defined, discussions around more expansive, potentially income-capped, forgiveness programs continue. While not guaranteed, the momentum towards broader relief suggests that 2026 could see the solidification of policies that move beyond existing program structures to offer more universal forms of debt cancellation.

The goal behind these changes for student loan forgiveness 2026 is multifaceted: to rectify past administrative errors, to make existing programs more accessible, and to provide a more equitable path to debt-free living for a significant portion of the borrowing population. Keeping abreast of these developments is key to understanding your potential for relief.

Who Qualifies? Eligibility Criteria for 1.5 Million Borrowers

The question on many borrowers’ minds is, “Do I qualify?” With 1.5 million borrowers targeted for relief under student loan forgiveness 2026, understanding the eligibility criteria is paramount. While specifics can vary based on the program, there are common threads and new considerations that will determine who benefits from these initiatives.

General Eligibility Factors

- Type of Loan: Generally, federal student loans are eligible for these programs. This includes Direct Loans (Stafford, PLUS, Consolidation) and FFEL Program loans, though FFEL loans often need to be consolidated into a Direct Consolidation Loan to qualify for certain benefits, especially for IDR and PSLF. Private student loans are almost never eligible for federal forgiveness programs.

- Repayment History: For IDR forgiveness, the length and consistency of your repayment history are crucial. The IDR account adjustment will retroactively count periods of repayment, as well as certain periods of deferment and forbearance, towards the 20- or 25-year forgiveness timeline.

- Employment (for PSLF): If pursuing PSLF, continuous full-time employment with a qualifying government or non-profit organization is a fundamental requirement.

- Income and Family Size (for IDR): Your adjusted gross income (AGI) and family size are primary determinants of your monthly payment amount under IDR plans, which in turn affects how long it takes to reach forgiveness.

Specifics for the IDR Account Adjustment

The IDR account adjustment is a significant driver of the anticipated student loan forgiveness 2026. Borrowers will receive credit for:

- Any months in repayment, regardless of the payment plan.

- Periods of 12 or more consecutive months in forbearance.

- Periods of 36 or more cumulative months in forbearance.

- Months spent in economic hardship or military deferment after 2013.

- Any time in repayment prior to consolidation on consolidated loans.

This adjustment is largely automatic for eligible federal loan borrowers, meaning many will not need to take explicit action to receive the credit. However, borrowers with commercially held FFEL loans or Perkins Loans may need to consolidate them into a Direct Consolidation Loan by a specific deadline (often in 2024 or 2025) to benefit from the adjustment. It’s critical to check official Department of Education announcements for the most current deadlines.

Navigating the Application Process and Key Deadlines

Even with automatic adjustments, understanding the application process and adhering to crucial deadlines is vital for maximizing your chances of receiving student loan forgiveness 2026. While some relief might be applied automatically, proactive engagement can ensure you don’t miss out on potential benefits.

Steps to Take Now

- Verify Your Loan Type: Log into your StudentAid.gov account to determine if you have federal Direct Loans, FFEL Program loans, or Perkins Loans. This is the foundational step for understanding your eligibility.

- Consolidate FFEL/Perkins Loans (If Applicable): If you have commercially held FFEL loans or Perkins Loans, you will likely need to consolidate them into a Direct Consolidation Loan to qualify for the IDR account adjustment and many other federal forgiveness benefits. There will be a deadline for this, so act swiftly once announced or when you confirm your loan type.

- Enroll in an IDR Plan: If you are not already on an Income-Driven Repayment plan, consider enrolling. While the IDR account adjustment will retroactively count past periods, being on an IDR plan ensures future payments continue to count towards forgiveness. The new SAVE Plan (Saving on a Valuable Education) is often the most beneficial IDR plan for many borrowers.

- Certify PSLF Employment Annually: For those pursuing Public Service Loan Forgiveness, it is crucial to certify your employment annually or whenever you change employers. This keeps your payment count accurate and reduces potential headaches down the line.

- Update Contact Information: Ensure your contact information (email, mailing address, phone number) is up-to-date with your loan servicer and on StudentAid.gov. This ensures you receive important notifications about your loan status and any forgiveness opportunities.

Important Deadlines to Watch For

While specific dates for student loan forgiveness 2026 initiatives are continually updated, here are general types of deadlines to be aware of:

- IDR Account Adjustment Consolidation Deadline: This is arguably the most critical deadline for borrowers with older, non-Direct federal loans. Missing this could mean missing out on significant retroactive payment counts.

- Annual IDR Recertification: Although currently paused for some, you will eventually need to recertify your income and family size annually for IDR plans to keep your payments affordable and your forgiveness timeline on track.

- PSLF Employment Certification: No hard deadline for this, but consistent, annual certification is highly recommended.

Always refer to official communications from the U.S. Department of Education and your loan servicer for the most accurate and up-to-date information on deadlines and requirements.

The Impact: What 1.5 Million Borrowers Can Expect

The anticipated relief for 1.5 million borrowers under student loan forgiveness 2026 represents a monumental shift in the financial landscape for a significant portion of the population. The impact extends beyond individual financial statements, potentially influencing broader economic trends and social mobility.

Individual Financial Freedom

For individuals, the most immediate and profound impact is the liberation from debt. This can lead to:

- Increased Disposable Income: Freed from monthly loan payments, borrowers will have more money for savings, investments, or discretionary spending.

- Improved Credit Scores: The removal of a significant debt obligation can positively impact credit scores, opening doors to better rates on mortgages, car loans, and other forms of credit.

- Major Life Milestones: Forgiveness can enable borrowers to achieve long-delayed goals, such as buying a home, starting a family, or pursuing further education without the shadow of past debt.

- Reduced Stress and Mental Health Benefits: The psychological burden of student loan debt is immense. Its removal can lead to significant improvements in mental well-being and overall quality of life.

Broader Economic and Social Implications

On a larger scale, the forgiveness for 1.5 million borrowers can contribute to:

- Economic Stimulus: Increased disposable income for millions can translate into greater consumer spending, stimulating local and national economies.

- Reduced Wealth Inequality: Student loan debt disproportionately affects certain demographic groups. Forgiveness can help reduce wealth disparities and promote more equitable economic opportunities.

- Workforce Mobility: With less debt, individuals may feel more empowered to pursue careers in lower-paying public service fields or entrepreneurial ventures, rather than being tied to high-paying jobs solely to service debt.

- Higher Education Accessibility: While not directly addressing college costs, a more manageable debt landscape might indirectly encourage future students, knowing that pathways to relief exist.

The ripple effect of student loan forgiveness 2026 is expected to be substantial, offering not just a temporary reprieve but a fundamental change in financial trajectory for those who qualify.

Potential Challenges and How to Overcome Them

While the prospect of student loan forgiveness 2026 is largely positive, borrowers should be aware of potential challenges and how to navigate them. The student loan system can be complex, and proactive engagement is often the key to success.

Common Hurdles Borrowers Face

- Information Overload and Misinformation: The sheer volume of information, combined with unofficial sources, can lead to confusion. Always rely on official government websites and your loan servicer for accurate information.

- Administrative Delays: Processing millions of accounts can take time. Be prepared for potential delays in seeing changes reflected in your account or receiving formal forgiveness notifications.

- Loan Servicer Changes: The student loan servicing landscape has seen frequent changes. If your servicer changes, ensure you set up new online accounts and confirm your information is transferred correctly.

- Tax Implications: While federal student loan forgiveness is currently tax-free through 2025, it’s crucial to understand potential tax implications for forgiveness received in 2026 and beyond, as state laws can vary. Consult a tax professional if you have concerns.

- Maintaining Eligibility: For ongoing programs like IDR or PSLF, it’s essential to continue meeting eligibility requirements, such as annual income recertification or qualifying employment.

Strategies for Overcoming Challenges

- Stay Informed: Regularly check StudentAid.gov and your loan servicer’s website for official updates. Subscribe to email newsletters from these sources.

- Keep Meticulous Records: Document all communications with your loan servicer, including dates, names of representatives, and summaries of conversations. Keep copies of all submitted applications and confirmation notices.

- Consolidate Early (If Needed): If you have non-Direct federal loans, consolidate them well before any announced deadlines to ensure they are processed in time for the IDR account adjustment.

- Seek Professional Advice: If you are unsure about your eligibility or the best path forward, consider consulting a non-profit student loan counselor or a financial advisor specializing in student debt.

- Be Patient but Persistent: While delays can be frustrating, persistence in following up and ensuring your applications are complete can make a difference.

By being prepared and proactive, borrowers can significantly reduce the likelihood of encountering setbacks and ensure they fully benefit from the opportunities presented by student loan forgiveness 2026.

The SAVE Plan: A Game Changer Leading into 2026

Among the various initiatives shaping student loan forgiveness 2026, the Saving on a Valuable Education (SAVE) Plan stands out as a particularly impactful Income-Driven Repayment (IDR) option. Launched to replace the Revised Pay As You Earn (REPAYE) plan, the SAVE Plan offers significant advantages that could accelerate forgiveness for many borrowers and make payments more affordable in the interim.

Key Features of the SAVE Plan

- Lower Monthly Payments: The SAVE Plan calculates monthly payments based on a smaller portion of your discretionary income. For undergraduate loans, payments are set at 5% of discretionary income, down from 10% on other IDR plans. For graduate loans, it remains 10%, and for those with both, it’s a weighted average.

- Higher Income Exemption: The amount of income considered non-discretionary is increased, meaning more of your income is protected from payment calculations. This effectively lowers your discretionary income and, consequently, your monthly payment.

- Interest Subsidy: A groundbreaking feature of the SAVE Plan is that if your calculated monthly payment doesn’t cover the accrued monthly interest, the government covers the remaining interest. This prevents your loan balance from growing due to unpaid interest, a common issue with other IDR plans.

- Earlier Forgiveness for Smaller Balances: For borrowers with original loan balances of $12,000 or less, forgiveness can occur after just 10 years of payments. For every additional $1,000 borrowed above that, an additional year of payments is required, up to the standard 20 or 25 years. This feature is a direct pathway to earlier student loan forgiveness 2026 for millions.

How the SAVE Plan Integrates with 2026 Forgiveness

The SAVE Plan is designed to work in tandem with the IDR account adjustment. Payments made under the SAVE Plan will count towards the forgiveness timeline, and the interest subsidy ensures that even if your payments are very low, your balance won’t balloon, making eventual forgiveness more impactful. For borrowers who enroll in SAVE, the combination of retroactive payment credit from the IDR adjustment and the favorable terms of the SAVE Plan can significantly shorten their path to debt relief by 2026 and beyond.

It’s highly recommended that any borrower struggling with federal student loan payments or seeking a path to forgiveness explore the SAVE Plan. Enrollment is straightforward through StudentAid.gov.

Looking Ahead: The Future of Student Loan Debt and Forgiveness

The reforms and initiatives culminating in student loan forgiveness 2026 are not necessarily the final word on student debt relief. The conversation around higher education affordability and student loan reform is ongoing, and future legislative or administrative actions could further shape the landscape.

Continued Advocacy and Policy Debates

Advocacy groups and policymakers continue to debate various approaches to student loan debt, from tuition-free college proposals to more expansive, across-the-board debt cancellation. While the current focus is on targeted relief and administrative improvements, these broader discussions could influence future policy decisions beyond 2026.

The Importance of Financial Literacy

Regardless of future policy, financial literacy remains paramount. Understanding how student loans work, the different repayment options, and the available forgiveness programs empowers borrowers to make informed decisions and navigate their financial journey effectively. Resources on StudentAid.gov offer valuable tools and information for borrowers at every stage.

Staying Engaged

For the 1.5 million borrowers poised to benefit from student loan forgiveness 2026, and for all others with student debt, staying engaged and informed is critical. The student loan environment is dynamic, and vigilance ensures you can adapt to changes and seize opportunities for relief as they arise.

This period marks a significant turning point for many, offering a genuine chance to shed the weight of student loan debt and build a more secure financial future. By understanding the programs, verifying eligibility, and taking proactive steps, borrowers can effectively navigate the path to forgiveness.

Conclusion: Seizing the Opportunity for Student Loan Forgiveness in 2026

The updates and expansions to student loan forgiveness programs leading into 2026 represent a beacon of hope for 1.5 million borrowers grappling with educational debt. From the retroactive benefits of the IDR account adjustment to the favorable terms of the SAVE Plan, the pathways to financial relief are becoming clearer and more accessible than ever before. This is a pivotal moment for borrowers to reassess their loan status, understand their options, and take decisive action.

The journey to student loan forgiveness 2026 requires diligence and a proactive approach. By verifying your loan types, consolidating when necessary, enrolling in appropriate repayment plans like SAVE, and staying informed through official channels, you can position yourself to receive the maximum benefit. The impact of this widespread forgiveness will not only transform individual lives by fostering financial freedom and reducing stress but also contribute to broader economic stability and social equity.

Do not let the complexity of the system deter you. The resources are available, and the intent behind these changes is to provide genuine relief. Take the time to review your situation, leverage the official guidance from StudentAid.gov, and consult with trusted advisors if needed. The promise of student loan forgiveness 2026 is within reach for millions, and understanding how to claim it is your first step towards a debt-free future. Seize this opportunity to redefine your financial trajectory and embrace the possibilities that come with true financial liberation.