Federal Reserve Interest Rate Decisions Early 2026: Analysis & Forecasts

Federal Reserve Interest Rate Decisions Early 2026: A Deep Dive into Monetary Policy and Economic Outlook

As we approach the horizon of early 2026, the financial world’s gaze remains firmly fixed on the Federal Reserve. The decisions made by the Federal Open Market Committee (FOMC) regarding interest rates have profound implications, shaping everything from mortgage rates and consumer lending to corporate investments and international trade. Understanding the trajectory of Federal Reserve rates 2026 is not merely an exercise for economists; it’s a critical component for businesses, investors, and everyday citizens planning their financial futures. This comprehensive analysis will explore the factors influencing the Fed’s decisions, project potential scenarios for early 2026, and discuss the likely impact on the broader economy.

The role of the Federal Reserve, as the central bank of the United States, is multifaceted, but its primary mandates are to promote maximum employment, stable prices, and moderate long-term interest rates. Achieving this delicate balance often involves navigating complex economic currents, anticipating future trends, and reacting to unforeseen global events. The period leading up to and including early 2026 is expected to be no different, with various domestic and international pressures potentially influencing the Fed’s stance on interest rates.

Understanding the Federal Reserve’s Mandate and Tools

Before delving into specific forecasts for Federal Reserve rates 2026, it’s essential to revisit the core principles guiding the Fed’s actions. The dual mandate of maximum employment and price stability often presents a trade-off, particularly during periods of economic flux. When inflation is high, the Fed typically raises interest rates to cool down the economy and curb rising prices. Conversely, during periods of low employment and sluggish growth, the Fed might lower rates to stimulate economic activity.

Key Economic Indicators Monitored by the Fed

The FOMC relies on a vast array of economic data to inform its decisions. These indicators provide a snapshot of the economy’s health and help forecast future trends:

- Inflation Data: The Personal Consumption Expenditures (PCE) price index is the Fed’s preferred measure of inflation. Core PCE, which excludes volatile food and energy prices, is particularly scrutinized. The Fed generally targets an average inflation rate of 2%. Deviations from this target significantly influence interest rate policy.

- Employment Statistics: The unemployment rate, non-farm payrolls, wage growth, and labor force participation rates are crucial for assessing the health of the labor market. A strong labor market typically indicates sustained economic growth, but also potential inflationary pressures.

- Gross Domestic Product (GDP): GDP growth figures provide an overall measure of economic output. Sustained strong growth might warrant higher interest rates to prevent overheating, while weak growth could lead to rate cuts.

- Consumer Spending and Business Investment: These metrics reflect demand within the economy. Robust consumer spending and business investment are signs of confidence and economic expansion.

- Global Economic Conditions: International economic developments, including global growth, geopolitical events, and commodity prices, can also impact the U.S. economy and, consequently, the Fed’s decisions.

The Fed’s Primary Tool: The Federal Funds Rate

The most prominent tool at the Fed’s disposal is the federal funds rate – the target rate for overnight lending between banks. While the Fed does not directly control this rate, it influences it through various policy instruments, primarily by adjusting the interest rate it pays on reserve balances held by banks and through its open market operations. Changes in the federal funds rate ripple through the financial system, affecting other interest rates, including prime rates, mortgage rates, and savings account yields. Therefore, when discussing Federal Reserve rates 2026, we are primarily referring to the projected path of the federal funds rate.

Economic Landscape Leading into Early 2026

Forecasting the economic landscape more than a year out is inherently challenging, as numerous variables can shift. However, based on current trends and expert consensus, several key themes are likely to dominate the economic narrative as we approach early 2026.

Inflationary Pressures: A Lingering Concern or Under Control?

The battle against inflation has been a defining feature of recent monetary policy. By early 2026, the expectation is that inflation will have moderated closer to the Fed’s 2% target. However, the path to this target is rarely smooth. Supply chain resilience, geopolitical stability, energy prices, and wage growth will all play a significant role. If inflation proves more stubborn than anticipated, the Fed may be compelled to maintain a higher-for-longer interest rate stance, directly impacting Federal Reserve rates 2026. Conversely, if inflation falls below target too rapidly, the Fed might consider easing monetary policy.

Labor Market Dynamics

The strength of the labor market is another critical determinant. A persistently tight labor market, characterized by low unemployment and strong wage growth, could fuel inflationary pressures. By early 2026, economists generally expect the labor market to have cooled somewhat from its peak tightness, but to remain relatively robust. Significant shifts, such as a sharp rise in unemployment or a substantial slowdown in wage growth, would undoubtedly influence the Fed’s interest rate decisions.

Economic Growth Trajectory

The U.S. economy’s growth trajectory will also be under intense scrutiny. A soft landing, where inflation is tamed without triggering a recession, is the ideal scenario. However, risks of a mild recession or a period of stagnating growth cannot be entirely dismissed. The Fed’s policy will be tailored to support sustainable growth while maintaining price stability. If growth slows considerably, the emphasis might shift towards supporting economic activity through lower rates.

Global Context and Geopolitical Risks

The interconnectedness of the global economy means that international events can have significant domestic repercussions. Geopolitical tensions, shifts in global trade policies, and economic performance in major trading partners (like Europe and Asia) can all influence the U.S. economic outlook. For instance, a global economic slowdown could dampen demand for U.S. exports, affecting domestic growth and potentially influencing the Fed’s approach to Federal Reserve rates 2026.

Projecting Federal Reserve Rates Early 2026: Scenarios and Possibilities

Given the multitude of influencing factors, projecting the exact path of Federal Reserve rates 2026 is challenging. However, we can outline several plausible scenarios based on current economic projections and the Fed’s stated objectives.

Scenario 1: Gradual Easing (Most Likely)

In this scenario, inflation continues its downward trend, gradually approaching the 2% target by late 2025 or early 2026. The labor market, while still healthy, shows signs of rebalancing, with wage growth moderating. Economic growth remains positive but perhaps below its long-term potential, avoiding an overheating economy. In this environment, the Fed would likely embark on a series of gradual interest rate cuts, aiming to normalize monetary policy without reigniting inflation. The federal funds rate might settle in a range considered more neutral, allowing for sustained economic expansion. This would mean Federal Reserve rates 2026 would be lower than current levels, but not necessarily back to pre-pandemic lows.

Scenario 2: Higher-for-Longer (Inflation Persistence)

This scenario assumes that inflation proves more persistent than anticipated, perhaps due to renewed supply chain disruptions, elevated energy prices, or stronger-than-expected wage growth. In this case, the Fed would be forced to maintain a ‘higher-for-longer’ interest rate policy to ensure inflation is brought firmly under control. Rate cuts, if they occur, would be modest and cautious, and the overall level of Federal Reserve rates 2026 would remain elevated compared to the gradual easing scenario. This could lead to a period of slower economic growth as higher borrowing costs impact consumer and business spending.

Scenario 3: Aggressive Cuts (Economic Downturn)

Should the U.S. economy experience a significant downturn or recession by late 2025 or early 2026, the Fed would likely react with more aggressive interest rate cuts. This would be a response to a sharp rise in unemployment and a significant contraction in economic activity. In this scenario, the priority would shift from fighting inflation to stimulating growth. Federal Reserve rates 2026 could see a rapid reduction, potentially approaching levels seen during previous economic crises, alongside other unconventional monetary policy tools if necessary.

Scenario 4: Limited Changes (Stagnant Economy)

A less likely but still possible scenario involves the economy entering a period of prolonged stagnation, characterized by low growth and inflation hovering around the Fed’s target. In such a situation, the Fed might opt for limited changes to interest rates, maintaining a relatively stable policy until a clearer direction emerges. This ‘wait and see’ approach would suggest that Federal Reserve rates 2026 might not see dramatic shifts in either direction, reflecting a lack of strong impetus for change.

Impact of Federal Reserve Rates 2026 on Various Sectors

The projected path of Federal Reserve rates 2026 will have far-reaching consequences across different sectors of the economy.

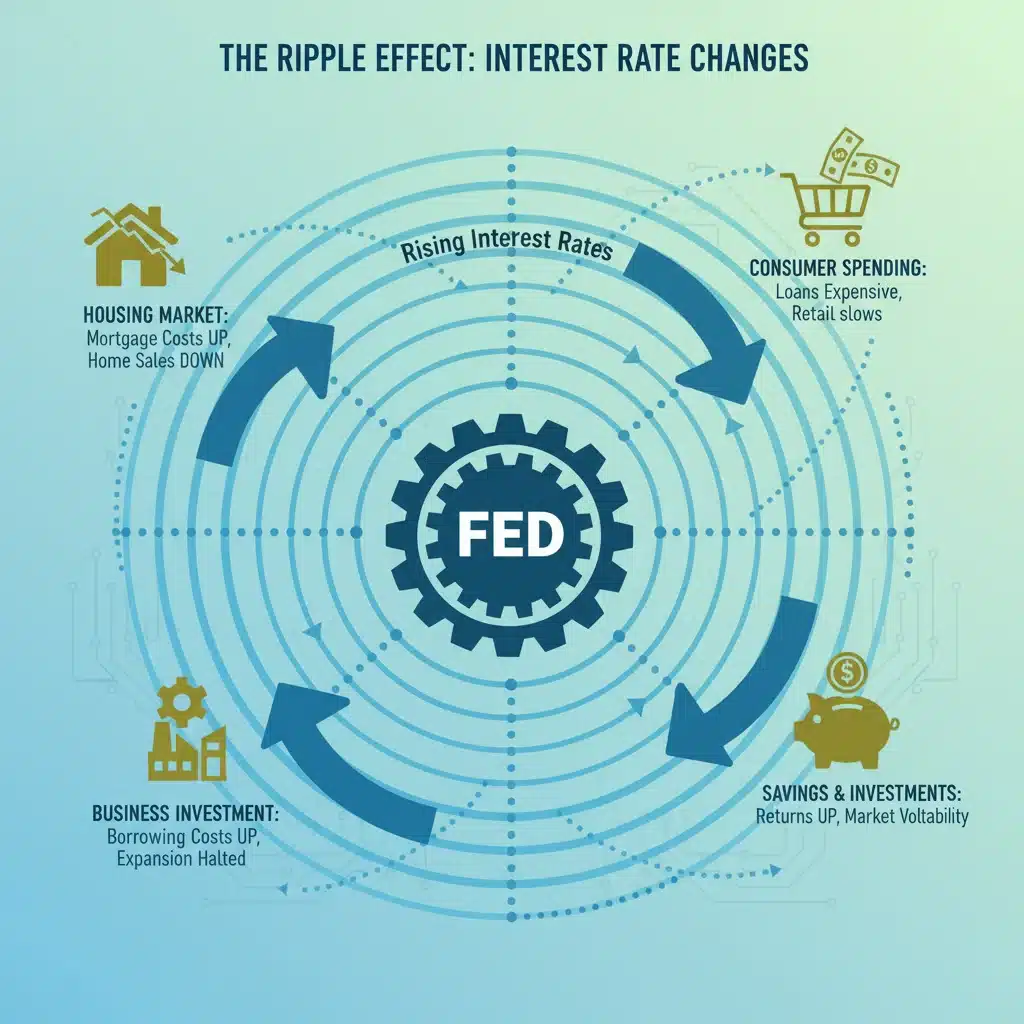

Housing Market

The housing market is particularly sensitive to interest rate changes. Lower rates typically lead to lower mortgage costs, making homeownership more affordable and stimulating demand. Conversely, higher rates can cool the market by increasing borrowing costs. If the Fed embarks on gradual rate cuts by early 2026, we could see a modest revival in housing activity and affordability. A ‘higher-for-longer’ scenario, however, would continue to exert pressure on affordability and potentially dampen sales.

Consumer Spending and Lending

Consumer spending, a major driver of the U.S. economy, is influenced by the cost of borrowing. Lower interest rates reduce the cost of credit card debt, auto loans, and personal loans, encouraging consumers to spend. Higher rates have the opposite effect, prompting consumers to save more and borrow less. The trajectory of Federal Reserve rates 2026 will therefore directly impact consumer confidence and discretionary spending patterns.

Business Investment and Corporate Borrowing

Businesses rely on borrowing to fund expansion, research and development, and operational needs. Lower interest rates reduce the cost of capital, making it more attractive for companies to invest and grow. Higher rates increase borrowing costs, potentially slowing down capital expenditure and hiring. The Fed’s policy in early 2026 will thus play a crucial role in shaping the investment climate and overall corporate profitability.

Financial Markets

Stock and bond markets are highly reactive to changes in interest rates and expectations about future Fed policy. Lower rates generally make bonds less attractive, pushing investors towards equities, and can also boost corporate earnings by reducing borrowing costs. Higher rates can make bonds more appealing and increase the discount rate used to value future corporate earnings, potentially putting downward pressure on stock prices. Investors will be closely watching the Fed’s signals for Federal Reserve rates 2026 to adjust their portfolios accordingly.

International Impact and the Dollar

The level of U.S. interest rates relative to other major global economies influences the strength of the U.S. dollar. Higher U.S. rates typically attract foreign investment, strengthening the dollar. A stronger dollar makes U.S. exports more expensive and imports cheaper. The Fed’s decisions in early 2026 could therefore have a significant impact on global trade balances and the competitiveness of U.S. industries on the international stage.

The Role of Forward Guidance and Communication

Beyond the actual rate decisions, the Federal Reserve’s communication – often referred to as ‘forward guidance’ – is a powerful tool. By clearly articulating its economic outlook and the likely path of future interest rates, the Fed aims to manage market expectations and reduce volatility. Statements from the FOMC, speeches by Fed officials, and the ‘dot plot’ (which illustrates individual FOMC members’ projections for the federal funds rate) are all scrutinized for clues about future policy. For Federal Reserve rates 2026, market participants will be paying close attention to any shifts in this guidance, as it can be as impactful as the rate decisions themselves.

Challenges and Uncertainties

Despite sophisticated models and extensive data analysis, forecasting economic conditions and monetary policy remains an art as much as a science. Several uncertainties could significantly alter the outlook for Federal Reserve rates 2026:

- Unforeseen Shocks: Geopolitical conflicts, natural disasters, or new health crises could disrupt supply chains, impact energy prices, or trigger sudden shifts in consumer behavior.

- Policy Lags: Monetary policy operates with significant lags, meaning the full effects of today’s decisions may not be felt for many months. This makes it challenging for the Fed to fine-tune its policy in real-time.

- Data Volatility: Economic data can be volatile and subject to revisions, sometimes paint a misleading picture of underlying trends.

- Market Expectations: If market expectations diverge significantly from the Fed’s intended path, it can create instability and complicate policy implementation.

Preparing for Federal Reserve Rates Early 2026

For individuals and businesses, understanding the potential trajectory of Federal Reserve rates 2026 is crucial for strategic financial planning. Here are some considerations:

- For Homeowners and Buyers: If gradual rate cuts are expected, those looking to buy a home might anticipate slightly more favorable mortgage rates. Existing homeowners with adjustable-rate mortgages should monitor rate movements closely.

- For Savers: In a higher-for-longer scenario, savings accounts and Certificates of Deposit (CDs) might continue to offer relatively attractive yields. If rates fall, these yields will likely decrease.

- For Investors: Diversification remains key. Consider how different asset classes (stocks, bonds, real estate) might perform under various interest rate scenarios. Consult with a financial advisor to align your investment strategy with your risk tolerance and financial goals.

- For Businesses: Companies should review their debt structures and consider refinancing opportunities if rates are expected to fall. Those planning significant capital expenditures should factor in the cost of borrowing.

Conclusion: Navigating the Future of Federal Reserve Rates 2026

The Federal Reserve’s interest rate decisions for early 2026 will be a critical determinant of the U.S. economic landscape. While a gradual easing of rates appears to be the most probable outcome, influenced by moderating inflation and a rebalancing labor market, the path is fraught with uncertainties. The Fed’s commitment to its dual mandate of price stability and maximum employment will continue to guide its actions, with every data point and policy statement meticulously analyzed by markets worldwide.

Staying informed about the latest economic indicators, understanding the Fed’s communication, and considering various potential scenarios are essential for navigating the financial environment of early 2026. Whether you are an investor, a business owner, or simply managing your personal finances, the future of Federal Reserve rates 2026 will undoubtedly play a significant role in shaping your economic reality. By remaining vigilant and adaptable, stakeholders can better position themselves to respond to the evolving monetary policy landscape and its broader economic implications.

The journey towards economic normalization is complex and dynamic. The Federal Reserve’s decisions will continue to be a linchpin, reflecting its ongoing efforts to steer the U.S. economy towards sustainable growth and stability. As we move closer to 2026, the clarity of these decisions will provide crucial guidance for all participants in the financial ecosystem.