Medicare Part B Savings 2026: Reduce Premiums Up to 15%

Understanding and managing healthcare costs in retirement is a critical aspect of financial planning for many Americans. For those enrolled in Medicare, particularly Medicare Part B, the monthly premiums can represent a significant expense. However, with strategic planning and a keen understanding of the rules, it’s entirely possible to achieve substantial Medicare Part B savings in 2026, potentially reducing your premiums by up to 15%.

This comprehensive guide is designed to empower you with the knowledge and actionable steps needed to navigate the intricacies of Medicare Part B and unlock these valuable savings. We’ll delve into the factors influencing your premiums, explore specific strategies to lower your costs, and provide a roadmap for proactive planning for 2026.

The Landscape of Medicare Part B Premiums

Before we dive into savings strategies, it’s essential to understand how Medicare Part B premiums are determined. Unlike Medicare Part A, which is typically premium-free for most beneficiaries, Part B requires a monthly premium. This premium covers outpatient care, doctor visits, preventive services, and other medically necessary services.

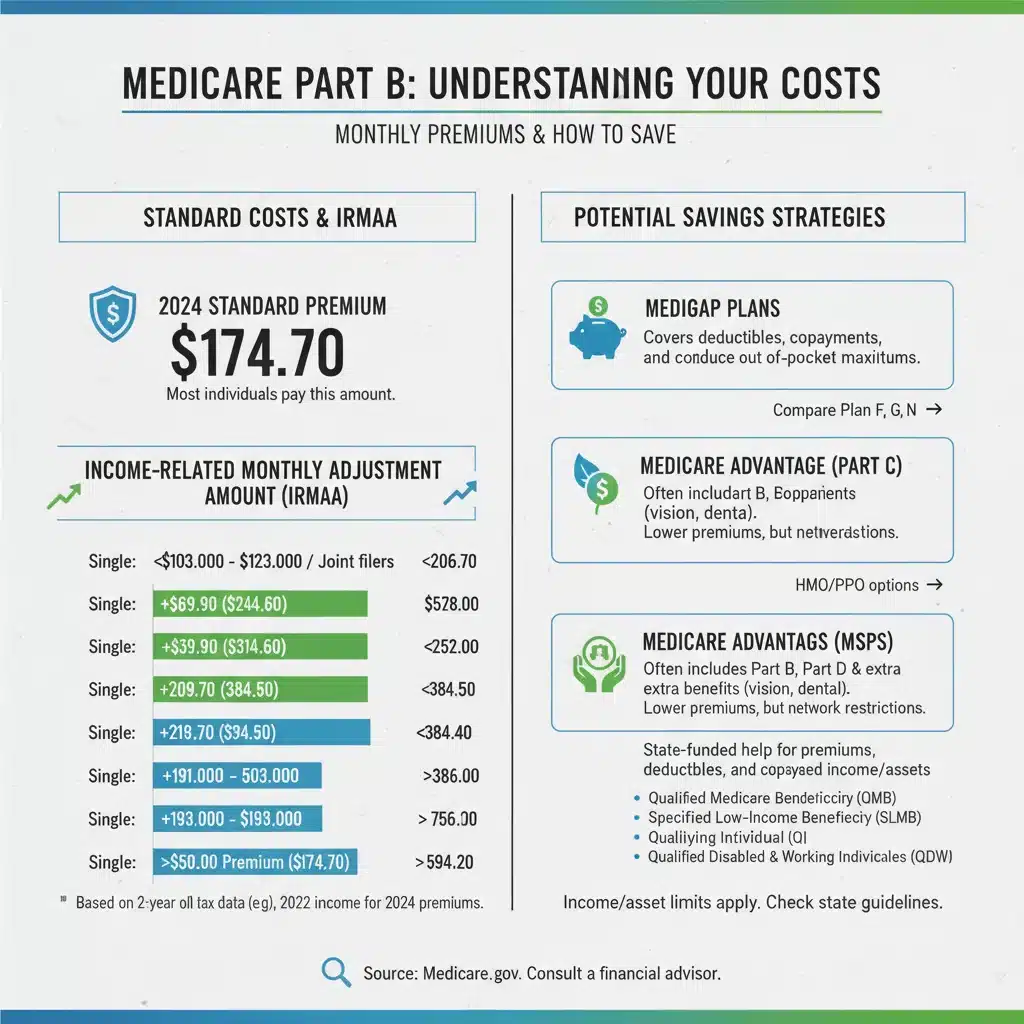

The standard Medicare Part B premium is set annually by the Centers for Medicare & Medicaid Services (CMS). However, not everyone pays the standard amount. A crucial factor influencing your premium is your income. This is where the Income-Related Monthly Adjustment Amount (IRMAA) comes into play.

Understanding IRMAA: The Income Factor

IRMAA is an additional amount you pay for Medicare Part B (and Part D) if your modified adjusted gross income (MAGI) exceeds certain thresholds. These thresholds are adjusted annually, and the income looked at is from two years prior. So, for your 2026 Medicare Part B premiums, the Social Security Administration (SSA) will primarily consider your 2024 tax return to determine if IRMAA applies.

The higher your MAGI, the higher your IRMAA, and consequently, the higher your Medicare Part B premium. This is why income planning is paramount for achieving significant Medicare Part B savings. Even a slight reduction in your MAGI can sometimes push you into a lower IRMAA bracket, leading to substantial savings.

Key Strategies for Medicare Part B Savings in 2026

Now that we understand the basics, let’s explore the concrete strategies you can employ to potentially reduce your Medicare Part B premiums by up to 15% or more in 2026.

1. Proactive Income Planning: Managing Your MAGI

This is arguably the most impactful strategy for Medicare Part B savings. Since your 2026 premiums are based on your 2024 income, you have a window of opportunity to influence your MAGI before it’s too late. Key considerations include:

- Tax-Efficient Retirement Withdrawals: If you’re retired or nearing retirement, consider the tax implications of your withdrawals from various accounts. Drawing heavily from traditional IRAs or 401(k)s can increase your MAGI. Conversely, Roth IRA withdrawals are generally tax-free and do not count towards MAGI for IRMAA purposes. A balanced withdrawal strategy that prioritizes Roth conversions or withdrawals before age 70.5 (when Required Minimum Distributions, or RMDs, begin) can be highly beneficial.

- Capital Gains Harvesting: Be mindful of capital gains from investments. Large capital gains can significantly inflate your MAGI. Consider strategies like tax-loss harvesting to offset gains or spreading out asset sales over multiple years.

- Timing of Income Events: If you have control over when certain income is realized (e.g., bonuses, severance packages, or exercising stock options), try to time these events to avoid pushing your MAGI over an IRMAA threshold in the year that will count for Medicare premium determinations.

- Qualified Charitable Distributions (QCDs): If you are 70½ or older, you can make qualified charitable distributions (QCDs) directly from your IRA to a qualified charity. These distributions count towards your RMD but are excluded from your taxable income, thus reducing your MAGI and potentially lowering your IRMAA.

- Delaying Social Security Benefits: While not directly reducing MAGI, delaying Social Security benefits can provide a larger monthly payment later, which can be part of a broader income strategy. However, remember that Social Security benefits are partially taxable, and these taxable portions do contribute to your MAGI.

2. Filing an IRMAA Appeal (Form SSA-44)

Even with careful income planning, sometimes life events occur that significantly reduce your income after the tax year used for IRMAA determination. In such cases, you may be eligible to appeal your IRMAA decision. This is a powerful tool for achieving Medicare Part B savings.

The Social Security Administration (SSA) allows you to request a new IRMAA determination if you’ve experienced a "life-changing event" that caused a significant reduction in your income. These events typically include:

- Marriage, divorce, or annulment

- Death of a spouse

- Work stoppage or reduction (e.g., retirement)

- Loss of income-producing property

- Loss of an employer pension

- Settlement from an employer or former employer

If you experience one of these events in 2025 (affecting your 2025 income, which would then be used to recalculate your 2026 premiums), or even in 2024 (which would affect your 2026 premiums based on the 2024 tax year), you can file Form SSA-44, "Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event." You will need to provide documentation to support your claim, such as pay stubs, retirement letters, or tax returns from the current year.

Key takeaway: Don’t just accept your IRMAA determination if your financial situation has changed. An appeal can lead to substantial Medicare Part B savings.

3. Exploring Medicare Advantage Plans (Part C) with Low or Zero Premiums

While Medicare Part B has a standard premium, you might find Medicare Advantage Plans (Part C) that offer a zero-dollar monthly premium beyond your Part B premium. These plans are offered by private companies approved by Medicare and cover all Part A and Part B services. Many also include additional benefits like prescription drug coverage (Part D), vision, dental, and hearing.

It’s crucial to understand that even with a zero-premium Medicare Advantage Plan, you still have to pay your Medicare Part B premium. However, some Advantage plans offer rebates on Part B premiums, effectively reducing your overall out-of-pocket costs. While not a direct reduction of the Part B premium itself, choosing the right Medicare Advantage plan can significantly lower your total healthcare expenses, providing an indirect form of Medicare Part B savings.

When considering a Medicare Advantage plan:

- Check the plan’s network: Ensure your preferred doctors and hospitals are in-network.

- Review out-of-pocket maximums: Understand the highest amount you could pay for covered services in a year.

- Compare benefits: Look for plans that offer benefits you will actually use, such as dental, vision, or fitness programs.

- Consider premium rebates: Some plans offer a "give back" or "rebate" on your Part B premium. These plans are particularly attractive for maximizing Medicare Part B savings.

4. State-Specific Medicare Savings Programs (MSPs)

For individuals with limited income and resources, Medicare Savings Programs (MSPs) can be a lifeline for achieving substantial Medicare Part B savings. These federal programs are administered by states and can help pay for Medicare Part A and/or Part B premiums, deductibles, coinsurance, and co-payments.

There are four main types of MSPs:

- Qualified Medicare Beneficiary (QMB) Program: Helps pay for Part A and Part B premiums, deductibles, coinsurance, and co-payments.

- Specified Low-Income Medicare Beneficiary (SLMB) Program: Helps pay for Part B premiums only.

- Qualifying Individual (QI) Program: Helps pay for Part B premiums only.

- Qualified Disabled and Working Individuals (QDWI) Program: Helps pay for Part A premiums for certain disabled individuals who lost premium-free Part A when they returned to work.

Each program has specific income and resource limits, which vary by state and are adjusted annually. If you qualify, an MSP could essentially cover your entire Medicare Part B premium, leading to 100% Medicare Part B savings on that expense. Contact your state Medicaid office or State Health Insurance Assistance Program (SHIP) for more information on eligibility and how to apply.

5. Strategic Use of Health Savings Accounts (HSAs)

If you were enrolled in a high-deductible health plan (HDHP) with an HSA before enrolling in Medicare, you might have accumulated significant tax-advantaged funds. While you cannot contribute to an HSA once enrolled in Medicare, you can still use the funds tax-free for qualified medical expenses, including Medicare Part B premiums (though not for Medigap premiums).

Using HSA funds for your Medicare Part B premiums effectively reduces your out-of-pocket costs, providing a form of Medicare Part B savings. This strategy is particularly powerful because the funds are tax-free when contributed, grow tax-free, and are withdrawn tax-free for qualified medical expenses.

Planning Timeline for 2026 Medicare Part B Savings

Effective planning is key to maximizing your Medicare Part B savings. Here’s a general timeline to consider:

- Early 2024: This is the income year that will primarily determine your 2026 IRMAA. Begin proactive income planning, considering tax-efficient withdrawals, capital gains, and any major income events.

- Late 2024/Early 2025: Review your 2024 tax return carefully. If your MAGI is close to an IRMAA threshold, or if you experienced a significant income reduction, start gathering documentation for a potential SSA-44 appeal.

- Fall 2025 (Annual Enrollment Period): This is your opportunity to review and switch Medicare Advantage plans or Part D plans. Look for plans with low or zero premiums, premium rebates, or additional benefits that reduce your overall healthcare spending.

- Late 2025: Social Security will typically send out IRMAA notices for 2026 in November or December. If you receive an IRMAA notification and believe it’s incorrect due to a life-changing event in 2024 or 2025, file your SSA-44 appeal promptly.

- Throughout 2025: If you believe you might qualify for a Medicare Savings Program, contact your state’s Medicaid office or SHIP for an eligibility assessment and to begin the application process.

Common Pitfalls to Avoid

While pursuing Medicare Part B savings, be aware of common mistakes that could cost you money:

- Ignoring IRMAA: Many beneficiaries are unaware of IRMAA or don’t realize their income could trigger it. Proactive planning is crucial.

- Not appealing IRMAA: If you have a life-changing event, don’t assume your IRMAA will automatically adjust. You must file an appeal.

- Missing enrollment periods: Late enrollment in Part B can lead to lifelong penalties, increasing your premiums. Ensure you enroll during your Initial Enrollment Period or a Special Enrollment Period if applicable.

- Focusing only on premiums: While crucial for Medicare Part B savings, remember to consider deductibles, co-pays, and out-of-pocket maximums when choosing plans. A low-premium plan isn’t always the cheapest overall if it has high out-of-pocket costs for services you use frequently.

- Not reviewing plans annually: Medicare plans change every year. What was a good plan last year might not be the best option for 2026. Always review your options during the Annual Enrollment Period.

The Role of Professional Guidance

Navigating Medicare and its associated costs can be complex. While this guide provides a solid foundation for achieving Medicare Part B savings, consulting with a qualified professional can offer personalized advice. Consider reaching out to:

- Financial Advisors: Especially those specializing in retirement planning, can help you strategize income management to minimize IRMAA.

- Tax Professionals: Can assist with understanding how your income and deductions affect your MAGI.

- State Health Insurance Assistance Program (SHIP): These programs offer free, unbiased counseling on all aspects of Medicare, including savings programs and plan comparisons.

Conclusion: Empowering Your Medicare Journey

Achieving significant Medicare Part B savings in 2026 is an attainable goal for many beneficiaries. By understanding how premiums are determined, proactively planning your income, exploring appeal options, considering Medicare Advantage plans with premium rebates, and leveraging state and federal assistance programs, you can significantly reduce your healthcare expenses.

The key is to be informed, proactive, and willing to explore all available avenues. Don’t wait until the last minute; begin your planning now to ensure you’re well-positioned to maximize your Medicare Part B savings for 2026 and beyond. Your financial well-being in retirement depends on it.

Remember, every dollar saved on premiums is a dollar that stays in your pocket, allowing you greater financial flexibility and peace of mind. Take control of your Medicare costs and secure your financial future.

Contributions for Retirement Growth")

in 2026: Catch-Up Limits, Investment Strategies & Future Planning")