Unlock 2026 Pell Grant Eligibility: Boost Your Award by 30% with Practical Steps

The 2026 Guide to Pell Grant Eligibility: Practical Steps for a 30% Higher Award (PRACTICAL SOLUTIONS)

Navigating the complex world of financial aid can often feel like deciphering an ancient text. For millions of students aspiring to achieve higher education, the Pell Grant stands as a beacon of hope, offering crucial financial assistance that doesn’t need to be repaid. As we look towards the 2026 academic year, understanding the nuances of Pell Grant Eligibility 2026 is more critical than ever. Significant changes to the Free Application for Federal Student Aid (FAFSA) process mean that what you knew about eligibility in previous years might no longer apply. This comprehensive guide is designed to empower you with the knowledge and practical steps needed not only to secure your Pell Grant but potentially increase your award by up to 30%.

The landscape of federal student aid is constantly evolving, and the 2026 cycle brings with it some of the most substantial reforms in decades. These changes aim to simplify the application process and expand eligibility, but without proper understanding, many students might miss out on the full benefits. Our goal is to demystify these changes, provide actionable advice, and ensure you are well-equipped to maximize your financial aid potential. From understanding the new Student Aid Index (SAI) to strategic financial planning, we’ll cover everything you need to know to optimize your Pell Grant Eligibility 2026.

Understanding the New FAFSA and Its Impact on 2026 Pell Grant Eligibility

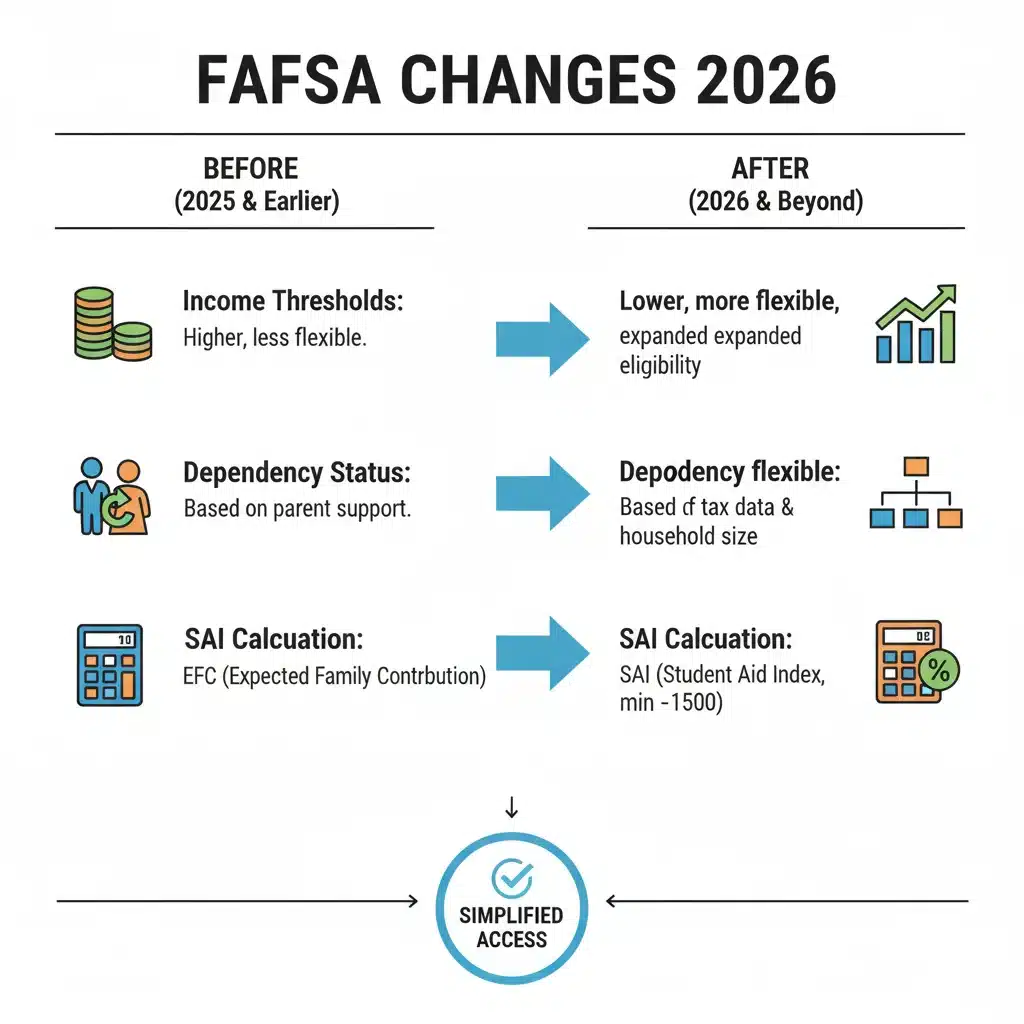

The FAFSA Simplification Act has ushered in a new era for federal student aid, and its full effects will be keenly felt in the 2026 cycle. The most significant change is the replacement of the Expected Family Contribution (EFC) with the Student Aid Index (SAI). While both are indices that determine a student’s financial need, the SAI calculation is designed to be more transparent and, in many cases, more generous. This shift is paramount for understanding Pell Grant Eligibility 2026.

The Shift from EFC to SAI: What You Need to Know

The EFC was often a source of confusion, as many families mistakenly believed it was the amount they would actually have to pay. The SAI, on the other hand, is an eligibility index that a college’s financial aid office uses to determine how much federal student aid a student is eligible to receive. A key difference is that the SAI can be a negative number (down to -1,500), indicating a very high level of financial need. This change is particularly beneficial for students from low-income backgrounds, potentially leading to higher Pell Grant awards.

Another critical aspect of the FAFSA overhaul is the streamlined application itself. The number of questions has been significantly reduced, making the process less daunting for applicants. However, fewer questions don’t mean less attention to detail. Accuracy remains key, as even minor errors can delay your application or impact your eligibility for the full Pell Grant amount.

Key FAFSA Changes Affecting 2026 Pell Grant Eligibility:

- Student Aid Index (SAI) Calculation: The formula for calculating financial need has been updated, with a greater emphasis on income and less on assets for many applicants. This can lead to a lower SAI for some, increasing their Pell Grant potential.

- Direct Data Exchange with IRS: The FAFSA will now directly import tax information from the IRS through a secure data exchange. This not only simplifies the process but also reduces errors and the need for manual verification. All contributors (student, spouse, parents) must consent to this data exchange for the FAFSA to be processed.

- Expanded Pell Grant Eligibility: The new FAFSA aims to expand Pell Grant eligibility to more students, particularly those with significant financial need. The maximum Pell Grant amount is tied to the federal poverty level, and the new SAI calculation can qualify more students for the maximum award.

- Changes to Family Size: The definition of family size will now be based on tax information provided through the direct data exchange with the IRS, rather than the previous FAFSA questions. This can impact the SAI calculation for some families.

- Small Business and Farm Net Worth: For families who own a small business or farm, the net worth of these assets must now be reported on the FAFSA. Previously, these were often excluded for small businesses. This change could potentially increase the SAI for some families.

- Child Support: Child support received will now be treated as an asset, not as untaxed income, which can also affect the SAI calculation.

Understanding these fundamental changes is the first step in strategically positioning yourself for maximum Pell Grant funding in 2026. The shift to SAI, the direct data exchange, and the new consideration of certain assets all play a crucial role in determining your final award.

Practical Steps to Maximize Your 2026 Pell Grant Award

Securing a Pell Grant is one thing; maximizing it to potentially achieve a 30% higher award is another. This requires proactive planning and a deep understanding of how your financial situation translates into eligibility. Here are actionable steps you can take:

1. File Your FAFSA Early and Accurately

This cannot be stressed enough. While the Pell Grant is an entitlement program (meaning if you qualify, you get it, regardless of when you apply), other forms of federal, state, and institutional aid are often first-come, first-served. Filing early ensures you’re considered for the broadest range of financial aid, which can indirectly impact your overall financial need and the perceived value of your Pell Grant.

- Meet Deadlines: Pay close attention to federal, state, and institutional FAFSA deadlines. Missing a deadline could mean missing out on significant aid.

- Gather Documents Early: Have all necessary tax documents (for both student and parents/spouse, if applicable), W-2s, bank statements, and investment records ready before you start the FAFSA.

- Double-Check Everything: Even with the direct data exchange, review all imported information for accuracy. Typos or incorrect entries can lead to delays or a miscalculation of your SAI.

2. Understand and Optimize Your Income and Assets

Your income and assets are primary drivers of your SAI. Strategic planning in the years leading up to your FAFSA application can significantly improve your Pell Grant Eligibility 2026.

- Income Management: If possible, consider ways to temporarily reduce taxable income in the year prior to applying for FAFSA. For example, if you or your parents are self-employed, managing deductible expenses can lower your Adjusted Gross Income (AGI).

- Asset Protection: Retirement accounts (401k, IRA, 403b) are generally not counted in the SAI calculation. If you have significant savings in non-retirement accounts, consider shifting them into retirement accounts if it aligns with your long-term financial goals and is done well in advance of the FAFSA application.

- 529 Plans: Funds in a 529 college savings plan owned by a dependent student or parent are considered a parental asset, which has a much lower impact on SAI than if owned by an independent student. If the 529 plan is owned by someone other than the student or parent (e.g., a grandparent), distributions from that plan will count as untaxed income to the student, which can significantly affect financial aid eligibility. It’s often advisable for grandparents to transfer ownership of a 529 plan to the parent of the beneficiary if they wish to avoid this impact.

- Small Business and Farm Net Worth: As mentioned, these are now included. If you own a small business or farm, consult with a financial advisor to understand how this change impacts your specific situation and if there are legitimate ways to optimize this reporting.

- Child Support Received: Remember, this is now an asset. Ensure it’s accurately reported.

3. Be Mindful of Your Dependency Status

Your dependency status (dependent vs. independent student) significantly impacts whose financial information is reported on the FAFSA. Independent students generally have a lower SAI because only their income and assets (and spouse’s, if applicable) are considered.

- Qualifying as an Independent Student: The criteria for being an independent student are specific and usually include being 24 years old by December 31st of the award year, being married, having dependents, being a veteran, being in graduate school, or being an emancipated minor or homeless youth. Understand these criteria thoroughly.

- Special Circumstances: If you have unusual circumstances that prevent you from providing parental information (e.g., parental abandonment, abuse), you can request a dependency override from your college’s financial aid office. This is a complex process but can be crucial for accessing aid.

4. Consider Professional Judgment and Special Circumstances

Life happens, and sometimes your current financial situation is not accurately reflected by the tax data from two years prior (which is what the FAFSA typically uses). The financial aid office at your chosen institution has the power of ‘professional judgment’ to adjust your financial aid package based on special circumstances.

- What Qualifies as Special Circumstances? This can include job loss, significant medical expenses not covered by insurance, divorce or separation of parents, death of a parent, or other substantial changes in income or assets since the tax year used on the FAFSA.

- How to Request a Review: Contact your college’s financial aid office directly. Be prepared to provide documentation (e.g., termination letters, medical bills, divorce decrees) to support your claim. This can potentially lower your SAI and increase your Pell Grant award.

5. Understand Your College’s Cost of Attendance (COA)

The Pell Grant amount you receive is also influenced by your college’s Cost of Attendance (COA). The Pell Grant cannot exceed your COA. While you can’t change the COA, understanding it helps you determine your overall financial need and how much of that need the Pell Grant will cover.

- Compare COAs: If you’re deciding between multiple institutions, compare their COAs. A lower COA might mean your Pell Grant covers a larger percentage of your overall expenses.

- Indirect Costs: Remember COA includes not just tuition and fees, but also housing, food, books, supplies, transportation, and personal expenses.

6. Maintain Satisfactory Academic Progress (SAP)

Once you receive a Pell Grant, you must maintain Satisfactory Academic Progress (SAP) to continue receiving it in subsequent years. Each institution defines SAP, but it typically includes:

- GPA Requirement: Maintaining a minimum cumulative GPA (e.g., 2.0 on a 4.0 scale).

- Pace of Completion: Successfully completing a certain percentage of attempted credits (e.g., 67%).

- Maximum Time Frame: Completing your degree within a specified maximum number of attempted credit hours (e.g., 150% of the credits required for your degree).

Failure to meet SAP can lead to the loss of all federal financial aid, including the Pell Grant. If you face challenges, communicate with your academic advisor and financial aid office immediately.

Common Pitfalls to Avoid for 2026 Pell Grant Eligibility

Even with the best intentions, applicants can make mistakes that jeopardize their Pell Grant Eligibility 2026. Being aware of these common pitfalls can help you avoid them:

1. Not Completing the FAFSA at All

This seems obvious, but many students, particularly those who think they won’t qualify, simply don’t bother. The FAFSA is the gateway to all federal aid, and often state and institutional aid as well. Even if your family’s income seems high, you might still qualify for some aid, especially with the new SAI calculation. Always apply!

2. Errors on the FAFSA

Despite the streamlined process and IRS data exchange, errors can still occur. Incorrect social security numbers, birth dates, or financial figures can cause significant delays or even lead to a rejection of your application. Review everything carefully before submitting.

3. Not Consenting to the IRS Data Exchange

With the FAFSA Simplification Act, all contributors (students, parents, spouse) must consent to the direct data exchange with the IRS. Without this consent, your FAFSA will not be processed, and you will not be eligible for federal student aid. Ensure everyone involved understands and provides their consent.

4. Misunderstanding Dependency Status

Incorrectly classifying yourself as an independent student when you are actually dependent, or vice-versa, can lead to your FAFSA being rejected or requiring extensive corrections. If you’re unsure, refer to the detailed questions on the FAFSA or consult with a financial aid advisor.

5. Ignoring Follow-Up Requests

Sometimes, the financial aid office may request additional documentation or clarification. Promptly responding to these requests is crucial. Delays can mean missed deadlines and lost aid opportunities.

6. Assuming You Won’t Qualify Based on Old Rules

The changes for 2026 are significant. Don’t let past assumptions about your eligibility deter you. The new SAI calculation and expanded Pell Grant eligibility criteria mean that more students will qualify, and some may qualify for higher amounts than before. Apply and see what you’re eligible for.

The 2026 Pell Grant and Beyond: Long-Term Financial Planning

While securing your 2026 Pell Grant is the immediate goal, it’s also an opportune moment to think about your long-term financial strategy for higher education. The Pell Grant is a fantastic foundation, but it often doesn’t cover the entire cost of attendance. Understanding how it fits into a broader financial plan is key.

Combining Pell Grants with Other Aid

The Pell Grant can be combined with various other forms of financial aid, including:

- State Grants: Many states offer their own grant programs based on financial need or academic merit. These often require FAFSA completion.

- Institutional Grants and Scholarships: Colleges and universities offer their own grants and scholarships. Some are need-based, others merit-based, and some are a combination. Always check with the financial aid office of each school you’re applying to.

- Private Scholarships: Countless organizations, foundations, and businesses offer private scholarships. These can be based on anything from academic achievement to specific talents, community service, or even unique hobbies. Dedicate time to searching for and applying to these.

- Federal Student Loans: While the goal is to minimize reliance on loans, federal student loans (subsidized and unsubsidized) offer benefits like fixed interest rates, income-driven repayment plans, and potential for loan forgiveness that private loans do not. They can bridge any remaining funding gaps after grants and scholarships.

- Work-Study Programs: Federal Work-Study provides part-time jobs for students with financial need, allowing them to earn money to help pay for educational expenses.

Developing a Budget for College

Even with a maximized Pell Grant, creating a realistic budget for your college years is essential. This includes:

- Tuition and Fees: The most obvious cost.

- Housing and Food: On-campus vs. off-campus living can significantly impact costs.

- Books and Supplies: These costs can add up quickly. Look for used books or digital versions.

- Transportation: Commuting costs, flights home, etc.

- Personal Expenses: Everything from toiletries to entertainment.

A well-planned budget helps you manage your funds, minimize debt, and focus on your studies.

Financial Literacy and Future Planning

Beyond securing aid, developing strong financial literacy skills will serve you well throughout college and beyond. Understanding concepts like budgeting, saving, debt management, and investing will empower you to make informed financial decisions. The experience of navigating Pell Grant Eligibility 2026 can be a starting point for a lifetime of smart financial choices.

Frequently Asked Questions About 2026 Pell Grant Eligibility

To further clarify any lingering questions, here are some frequently asked questions regarding the 2026 Pell Grant cycle:

Q1: What is the maximum Pell Grant award for 2026?

A1: The maximum Pell Grant award is determined annually by Congress. While the exact amount for 2026 has not yet been finalized, it is expected to be announced closer to the FAFSA opening for that cycle. For reference, the maximum award for the 2023-2024 academic year was $7,395. The FAFSA Simplification Act aims to expand eligibility for the maximum award to more students.

Q2: How is the Student Aid Index (SAI) calculated for 2026?

A2: The SAI calculation for 2026 will primarily be based on your (and your parents’ or spouse’s, if applicable) Adjusted Gross Income (AGI), untaxed income, and certain assets reported on your FAFSA. Key changes include the direct data exchange with the IRS, the inclusion of small business and farm net worth, and child support received being treated as an asset. The formula is designed to be more equitable and can result in a negative SAI for those with the highest need.

Q3: Does my family’s home equity count towards my assets for Pell Grant eligibility?

A3: No, the equity in your primary residence is not counted as an asset in the FAFSA calculation for Pell Grant Eligibility 2026. This remains a significant advantage for homeowners when determining financial need.

Q4: What if my financial situation changes after I submit my FAFSA?

A4: If you experience a significant change in financial circumstances (e.g., job loss, divorce, high medical expenses) after submitting your FAFSA, you should contact the financial aid office at your college. They have the authority to exercise ‘professional judgment’ and may adjust your SAI, potentially increasing your Pell Grant amount or other aid.

Q5: Can I receive a Pell Grant if I’m attending part-time?

A5: Yes, you can receive a Pell Grant if you are attending college part-time. However, your award amount will be prorated based on your enrollment intensity. For example, if you are enrolled half-time, you would typically receive half of the amount you would be eligible for if enrolled full-time.

Q6: Is there a limit to how many years I can receive a Pell Grant?

A6: Yes, students are generally eligible to receive a Pell Grant for no more than 12 semesters or the equivalent (roughly six years of full-time study). This is often referred to as your ‘Pell Grant Lifetime Eligibility Used’ (LEU).

Q7: How can I check my Pell Grant eligibility and award amount?

A7: After you submit your FAFSA, you will receive a FAFSA Submission Summary (FSS), which will indicate your Student Aid Index (SAI) and estimated Pell Grant eligibility. Your college’s financial aid office will then use this information to determine your actual award amount and include it in your financial aid offer letter.

Conclusion: Your Path to Maximizing 2026 Pell Grant Eligibility

The journey to higher education is a significant investment, and the Pell Grant remains a cornerstone of federal financial aid, making college accessible for millions. By understanding the critical changes introduced by the FAFSA Simplification Act, proactively managing your financial profile, and diligently completing your application, you are well on your way to optimizing your Pell Grant Eligibility 2026.

Remember, the key to potentially boosting your Pell Grant award by 30% or more lies in early and accurate FAFSA submission, strategic financial planning, and an awareness of the new SAI calculation. Don’t hesitate to leverage the resources available at your college’s financial aid office and seek professional advice if your situation is complex. With these practical steps, you can confidently navigate the financial aid process and secure the funding you need to achieve your academic dreams.

Start preparing now, gather your documents, and be ready to submit your FAFSA as soon as it becomes available for the 2026 academic year. Your future in higher education is within reach!