Federal vs. Private Student Loans 2026: Which Option Saves You 2.5% Annually?

As the academic year 2026 approaches, prospective students and their families face the perennial challenge of financing higher education. The landscape of student loans, broadly divided into federal and private options, presents a complex array of choices, each with its own set of interest rates, terms, and borrower protections. Understanding the nuances between these two categories is not merely an academic exercise; it’s a critical financial decision that can impact your long-term economic well-being. This comprehensive guide aims to dissect the intricacies of federal student loans and private student loans for 2026, with a keen focus on interest rates, potential savings, and the factors that should influence your borrowing decisions. Our goal is to help you determine which option, if any, could realistically save you around 2.5% annually, a significant figure over the life of a loan.

The cost of college continues to climb, making student loans an indispensable tool for millions. However, not all loans are created equal. The interest rate on your student loan is arguably the most critical factor, as it directly determines the total cost of borrowing. A seemingly small difference in the annual percentage rate (APR) can translate into thousands of dollars in savings or additional debt over a decade or more. For 2026, economic forecasts suggest a dynamic interest rate environment, making careful consideration of both federal and private offerings more important than ever.

This article will delve deep into the characteristics of each loan type, providing up-to-date insights into projected interest rates for 2026. We will explore the eligibility criteria, application processes, and, crucially, the repayment terms and borrower protections that differentiate federal from private loans. By the end of this read, you will be equipped with the knowledge to make an informed decision, ensuring you select the most advantageous student loan rates 2026 has to offer for your unique financial situation.

Understanding Student Loan Rates: A Primer for 2026

Before we compare specific loan types, it’s essential to grasp the fundamentals of how student loan rates are determined and what they mean for your borrowing experience. Interest rates are essentially the cost of borrowing money, expressed as a percentage of the loan amount. They can be fixed or variable, a distinction that carries significant implications for your repayment strategy.

Fixed vs. Variable Interest Rates

- Fixed Interest Rates: These rates remain constant throughout the life of the loan. This means your monthly payments will be predictable, offering stability and ease of budgeting. Federal student loans exclusively offer fixed interest rates, a key advantage for many borrowers. For student loan rates 2026, fixed rates provide certainty in an uncertain economic climate.

- Variable Interest Rates: These rates can fluctuate over time, typically in response to market indexes like the prime rate or LIBOR (though LIBOR is being phased out in favor of SOFR). While variable rates might start lower than fixed rates, they can increase, leading to higher monthly payments. Private student loans often offer both fixed and variable rate options. The potential for lower initial payments can be tempting, but the risk of future increases requires careful consideration, especially for long repayment periods.

Annual Percentage Rate (APR)

The APR is a broader measure of the cost of borrowing, encompassing not just the interest rate but also any fees associated with the loan. When comparing loan offers, always look at the APR to get a true sense of the total cost. A lower interest rate might look appealing, but high fees could make the overall APR less competitive. This is crucial when evaluating student loan rates 2026 from various lenders.

Factors Influencing Interest Rates in 2026

Several macroeconomic and individual factors influence student loan interest rates:

- Federal Funds Rate: Set by the Federal Reserve, this rate indirectly influences all lending rates, including student loans. Expectations for the Federal Funds Rate in 2026 will play a significant role.

- Inflation: Higher inflation generally leads to higher interest rates as lenders seek to maintain the real value of their returns.

- Economic Growth: A strong economy can lead to higher demand for loans and potentially higher rates, while a weaker economy might see rates decline.

- Creditworthiness (for Private Loans): For private student loans, your credit score and history (or that of a co-signer) are paramount. A higher credit score signals lower risk to lenders, often resulting in lower interest rates.

- Loan Type and Term: Different loan types (e.g., subsidized vs. unsubsidized federal loans, or different private loan products) will have varying rates. The length of the repayment term can also influence the rate.

Understanding these foundational concepts is the first step toward making an educated decision about your student loan options for 2026 and beyond.

Federal Student Loans: Stability, Benefits, and Projected 2026 Rates

Federal student loans are offered by the U.S. Department of Education and are widely considered the first and best option for most students due to their borrower-friendly terms and protections. They come with fixed interest rates, which are set annually by Congress. While we don’t have the exact student loan rates 2026 yet, we can project based on historical trends and current economic forecasts.

Types of Federal Student Loans

The primary types of federal student loans include:

- Direct Subsidized Loans: Available to undergraduate students with demonstrated financial need. The government pays the interest while you’re in school at least half-time, during your grace period, and during deferment.

- Direct Unsubsidized Loans: Available to undergraduate and graduate students, regardless of financial need. Interest accrues from the moment the loan is disbursed.

- Direct PLUS Loans: Available to graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS). These require a credit check, but the criteria are less stringent than for private loans.

Key Benefits of Federal Student Loans

Beyond fixed interest rates, federal loans offer a suite of benefits unmatched by private lenders:

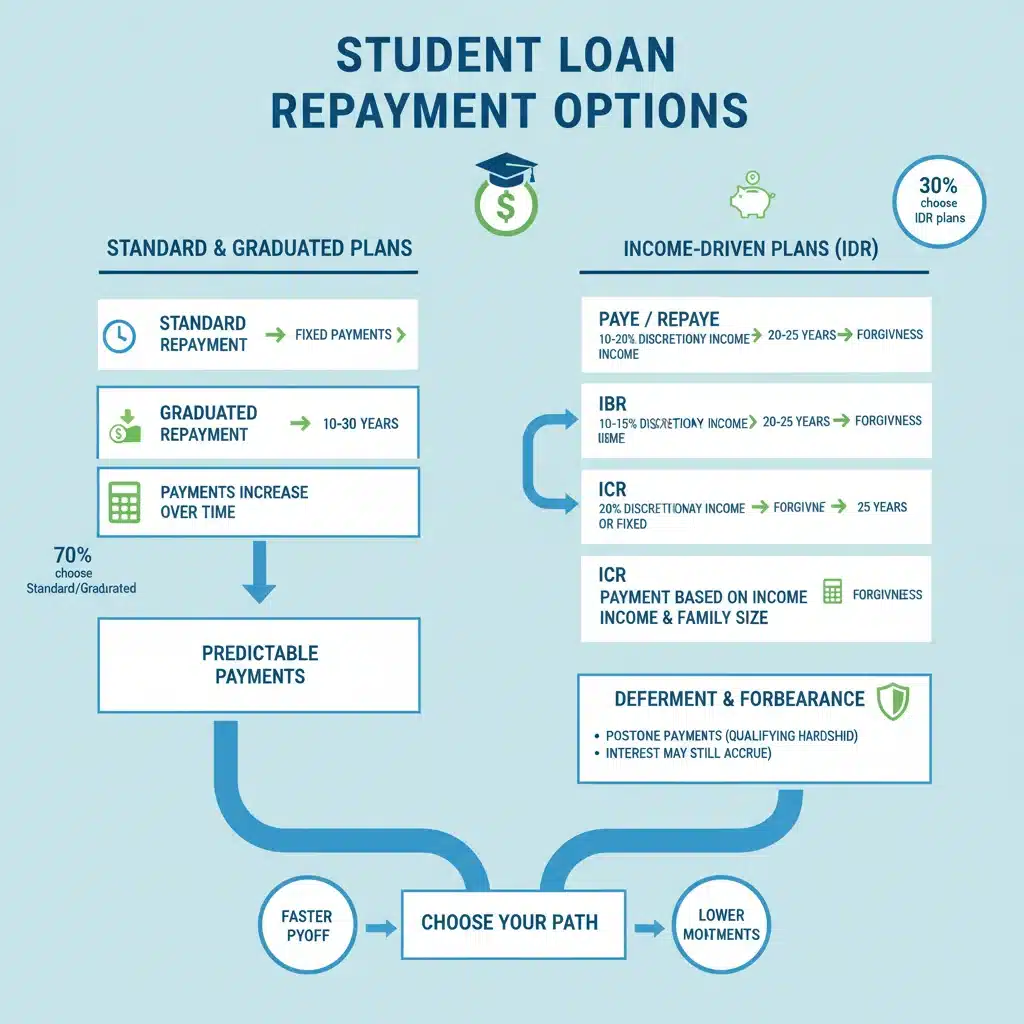

- Income-Driven Repayment (IDR) Plans: Payments are adjusted based on your income and family size, potentially making them more affordable. After 20 or 25 years (depending on the plan), any remaining balance may be forgiven.

- Deferment and Forbearance: Options to temporarily postpone or reduce payments if you’re facing financial hardship, unemployment, or other qualifying circumstances.

- Public Service Loan Forgiveness (PSLF): Forgiveness of the remaining loan balance after 120 qualifying monthly payments while working full-time for a qualifying non-profit organization or government agency.

- No Credit Check (for most loans): Direct Subsidized and Unsubsidized Loans do not require a credit check, making them accessible to students without established credit histories.

- Loan Consolidation: The ability to combine multiple federal loans into a single Direct Consolidation Loan, potentially simplifying repayment and unlocking additional IDR options.

Projected Federal Student Loan Rates for 2026

Federal student loan interest rates are set by federal law and are tied to the 10-year Treasury note yield. They are typically finalized in late spring for loans disbursed for the upcoming academic year. While it’s impossible to predict the exact rates for 2026, we can analyze current trends and expert predictions.

For the 2023-2024 academic year, interest rates were:

- Direct Subsidized and Unsubsidized Loans for undergraduates: 5.50%

- Direct Unsubsidized Loans for graduate students: 7.05%

- Direct PLUS Loans: 8.05%

Considering potential economic shifts and inflation, it is reasonable to expect student loan rates 2026 for federal loans to hover around these figures, possibly with slight increases if inflation remains elevated or the Federal Reserve continues its tightening policies. However, the fixed nature of these rates ensures that once you take out a federal loan, that rate will not change, offering invaluable predictability.

The stability and robust borrower protections of federal student loans often make them the most financially prudent choice, even if their initial interest rate might appear slightly higher than some private loan offers. The long-term security and flexibility they provide can easily outweigh a marginal rate difference.

Private Student Loans: Flexibility, Risk, and Expected 2026 Rates

Private student loans are offered by banks, credit unions, and other private lenders. Unlike federal loans, they are not guaranteed by the government and typically have fewer borrower protections. They are often used to bridge the gap between the cost of attendance and what federal aid, scholarships, and savings can cover.

How Private Student Loans Work

Private lenders assess your creditworthiness (or that of a co-signer) to determine your eligibility and interest rate. This means students with excellent credit scores and a stable financial history will qualify for the best rates, while those with limited or poor credit may struggle to get approved or face very high interest rates. Most undergraduate students will need a co-signer to qualify for competitive private student loan rates 2026.

Key Characteristics of Private Student Loans

- Credit-Based Eligibility: Approval and interest rates are heavily dependent on your credit score and history.

- Variable or Fixed Rates: Most private lenders offer both options. Variable rates can be lower initially but carry the risk of increasing over time.

- Fewer Borrower Protections: Private loans generally lack the income-driven repayment plans, extensive deferment/forbearance options, and forgiveness programs available with federal loans.

- Limited Repayment Flexibility: Repayment terms are typically less flexible than federal loans.

- No Loan Limits (Potentially): While federal loans have annual and aggregate limits, private loans may allow you to borrow up to the full cost of attendance, though this can lead to excessive debt.

Projected Private Student Loan Rates for 2026

Private student loan rates are tied to market indexes like the prime rate or SOFR (Secured Overnight Financing Rate). These rates are highly sensitive to the Federal Reserve’s monetary policy and broader economic conditions. Given the current economic environment and potential future rate hikes, we can anticipate that student loan rates 2026 for private loans will likely remain competitive but could also see upward pressure.

As of late 2023 and early 2024, private student loan rates for borrowers with excellent credit typically range from:

- Variable Rates: 6.00% to 14.00%+ APR

- Fixed Rates: 7.00% to 15.00%+ APR

It’s crucial to understand that these are ranges. The actual rate you receive will depend heavily on your credit score, the lender, and the loan term. For 2026, if economic conditions stabilize or the Federal Reserve begins to lower rates, we might see the lower end of these ranges become more accessible. Conversely, continued inflation and rate hikes could push rates higher. The 2.5% annual savings mentioned in the title would likely come from a comparison between a well-qualified borrower securing a low private rate versus the standard federal rate, or vice versa, depending on market conditions and individual credit profiles.

The 2.5% Annual Savings Scenario: Federal vs. Private Loan Rates 2026

The question of saving 2.5% annually is highly dependent on individual circumstances and the prevailing interest rate environment for student loan rates 2026. Let’s break down how this might occur.

Scenario 1: Federal Loans Offer Better Savings

In many cases, federal student loans will offer the more advantageous terms, even if their nominal interest rate is slightly higher than the lowest private loan rates. The value of federal loan benefits — particularly income-driven repayment plans, deferment, forbearance, and potential forgiveness — can far outweigh a 1-2% difference in interest rate, especially for borrowers who anticipate career paths with lower initial salaries or those who might face financial hardship.

For example, if federal loans offer a fixed rate of 5.5% for undergraduates, and the lowest private fixed rate you can qualify for is 7.5%, then federal loans are already saving you 2% annually. Add in the value of not paying interest while in school (for subsidized loans) or the safety net of IDR plans, and the effective savings can easily exceed 2.5% over the life of the loan, even if the initial rate difference is smaller.

Scenario 2: Private Loans Offer Better Savings (for exceptional borrowers)

There are specific, albeit rarer, situations where a private loan might offer a better deal. This typically applies to borrowers (or their co-signers) with impeccable credit scores (e.g., 750+), a very stable income, and a strong preference for a shorter repayment period. Such borrowers might qualify for a private loan with a variable or even fixed interest rate that is significantly lower than the federal offerings for 2026.

For instance, if federal PLUS loans are at 8.05% and a private lender offers an exceptional borrower a fixed rate of 5.55% (a 2.5% difference), then the private loan would indeed offer annual savings on interest. However, this scenario comes with a significant caveat: these borrowers are often those least likely to need the robust protections offered by federal loans. They are confident in their ability to repay quickly and have a strong financial safety net. It is absolutely critical for these borrowers to weigh the lower interest rate against the loss of federal protections. For most students, relying solely on a potentially lower private rate without considering the associated risks is not advisable.

The Hidden Costs and Benefits

When comparing student loan rates 2026, it’s crucial to look beyond the advertised APR:

- Origination Fees: Federal loans often have origination fees (e.g., around 1% for Direct Loans, 4% for PLUS Loans), which are deducted from the loan disbursement. Private loans may or may not have these fees. Always factor them into the true cost.

- Repayment Flexibility: The ability to pause payments or reduce them during hardship (federal loans) has immense financial value that isn’t captured in an interest rate.

- Potential for Forgiveness: PSLF and IDR forgiveness programs can wipe out significant debt, representing massive savings that no private loan can offer.

Therefore, while a direct 2.5% interest rate difference might be achievable in specific private loan scenarios for highly qualified borrowers, the overall financial advantage, especially for the average student, often lies with the comprehensive benefits and stability of federal student loans.

Making Your Decision: A Step-by-Step Approach for 2026

Choosing between federal and private student loans for 2026 requires a structured approach. Here’s a recommended process:

Step 1: Maximize Federal Student Aid First

Always start by completing the Free Application for Federal Student Aid (FAFSA). This is the gateway to all federal student loans, grants, and many scholarships. You won’t know your eligibility for federal aid until you complete it. Accept all grants and scholarships first, as this is money you don’t have to repay.

Step 2: Understand Your Federal Loan Offer

Review the types and amounts of federal loans you’ve been offered. Pay close attention to whether they are subsidized or unsubsidized, and their respective interest rates for the 2026-2027 academic year. Understand the origination fees associated with each loan.

Step 3: Calculate Your Funding Gap

Determine how much money you still need after exhausting all federal aid, grants, scholarships, and personal savings. This is your funding gap.

Step 4: Consider a Co-signer (for Private Loans)

If you anticipate needing private loans to cover your funding gap, having a creditworthy co-signer (e.g., a parent or guardian with excellent credit) can significantly improve your chances of approval and help you secure lower interest rates. This is especially true for undergraduate students with little to no credit history.

Step 5: Shop Around for Private Loans

If private loans are necessary, don’t settle for the first offer. Compare interest rates (both fixed and variable), fees, and repayment terms from multiple lenders. Use online comparison tools to get pre-qualified without impacting your credit score. Pay close attention to the APR, not just the interest rate, to understand the true cost of borrowing. Look specifically for the most competitive student loan rates 2026.

Step 6: Weigh the Pros and Cons

Create a simple comparison chart:

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Interest Rate Type | Fixed | Fixed or Variable |

| Borrower Protections | Extensive (IDR, Deferment, Forbearance, Forgiveness) | Limited |

| Credit Check | No (for most) | Yes (crucial) |

| Origination Fees | Yes, typically | Varies by lender |

| Loan Limits | Yes | No (potentially up to COA) |

Step 7: Borrow Only What You Need

Regardless of the loan type, borrow the absolute minimum necessary to cover your educational expenses. Every dollar borrowed accrues interest, increasing your total debt burden. Over-borrowing can lead to significant financial strain after graduation.

Step 8: Stay Informed

Keep an eye on economic news and official announcements regarding student loan rates 2026. Interest rates can shift, and new policies might be introduced that could affect your borrowing decisions.

Long-Term Implications of Your Loan Choice

The choice between federal and private student loans extends far beyond the immediate interest rate. The long-term implications can significantly affect your financial freedom and life choices after graduation.

Impact on Financial Health

High student loan debt can delay major life milestones such as buying a home, starting a family, or even saving for retirement. The type of loan you choose dictates your flexibility in managing this debt. Federal loans, with their IDR plans, offer a crucial safety net. If your income is lower than expected, these plans can prevent default and protect your credit score. Private loans, lacking these protections, can quickly become unmanageable if you face unemployment or underemployment.

Credit Score and Future Borrowing

Defaulting on any loan, especially a student loan, can severely damage your credit score, making it difficult to secure loans for a car, house, or even rent an apartment in the future. Federal loan protections are designed to help you avoid default, even in challenging circumstances. Private lenders are typically less forgiving.

Peace of Mind

The predictability of fixed federal interest rates and the availability of robust repayment options can provide significant peace of mind. Knowing that your payments can adjust if your income drops, or that you have options like deferment if you return to school, can alleviate a great deal of stress. This peace of mind often outweighs the allure of a slightly lower variable rate from a private lender that could spike unexpectedly.

The Value of Flexibility

Life after college is unpredictable. Your first job might not pay as much as you hoped, or you might decide to pursue further education or a public service career. Federal loans are designed with this flexibility in mind. Private loans, by contrast, offer a much more rigid repayment structure, which can be problematic if your post-graduation plans don’t unfold as expected.

Conclusion: Prioritizing Protection Over Potentially Lower Rates for Student Loan Rates 2026

For most students and families navigating the complexities of financing higher education in 2026, federal student loans remain the superior choice. While it’s tempting to chase the lowest advertised interest rate, especially when considering the possibility of saving 2.5% annually, the comprehensive benefits and borrower protections offered by federal loans often provide far greater long-term financial security and flexibility.

The fixed interest rates of federal loans offer predictability, shielding you from market fluctuations. More importantly, the suite of repayment options — including income-driven plans, deferment, forbearance, and various forgiveness programs — creates an essential safety net that private loans simply do not replicate. These protections are invaluable, especially in an unpredictable economic climate or if your post-graduation income is lower than anticipated.

Private student loans can serve a purpose as a supplemental funding source once federal options have been exhausted. For a very select group of borrowers with exceptional credit and stable financial outlooks, a private loan might present a marginally lower interest rate. However, even in these niche cases, the trade-off of losing federal protections must be thoroughly understood and accepted.

As you plan for 2026, prioritize filling out the FAFSA, understanding your federal aid package, and only then exploring private loan options to cover any remaining funding gaps. Always compare not just the student loan rates 2026 but the entire package of terms, fees, and borrower benefits. Making an informed decision now will empower you to manage your student debt effectively and achieve your educational and financial goals with greater confidence.

Remember, the goal is not just to secure a loan, but to secure the right loan — one that supports your academic journey without becoming an insurmountable financial burden. By carefully evaluating federal versus private student loan options, you can make a choice that truly saves you money and provides peace of mind throughout your repayment journey.